Tutorial 2: ScipyOptimizer Tutorial#

This tutorial demonstrates how to use the ScipyOptimizer from BrainTools for gradient-based optimization. The ScipyOptimizer provides a convenient wrapper around SciPy’s optimization methods with automatic differentiation via JAX, support for complex parameter structures, and seamless integration with BrainUnit quantities.

Introduction and Setup#

The ScipyOptimizer is designed for gradient-based optimization where derivatives can be computed automatically via JAX. It’s particularly useful for:

Smooth, differentiable objective functions

Neural network parameter optimization

Physics-based models with analytical gradients

Problems where gradient information is reliable

Key advantages over derivative-free methods:

Faster convergence for smooth problems

Higher precision solutions

Automatic gradients via JAX

Mature algorithms from SciPy

Let’s start by importing the necessary libraries:

# Core imports

import jax

import jax.numpy as jnp

import numpy as np

import matplotlib.pyplot as plt

from scipy.optimize import OptimizeResult

# BrainTools imports

import braintools as bts

import brainunit as u

import brainstate as bst

# Set up plotting

plt.style.use('default')

plt.rcParams['figure.figsize'] = (10, 6)

print("BrainTools version:", bts.__version__)

print("JAX version:", jax.__version__)

BrainTools version: 0.0.12

JAX version: 0.7.1

First, let’s check if SciPy is installed (it’s required for the optimizer to work):

try:

import scipy

from scipy.optimize import minimize

print(f"SciPy version: {scipy.__version__}")

print("✓ SciPy is available")

except ImportError:

print("❌ SciPy is not installed. Please install it with:")

print(" pip install scipy")

raise

SciPy version: 1.14.1

✓ SciPy is available

Basic Usage: Scalar Parameters#

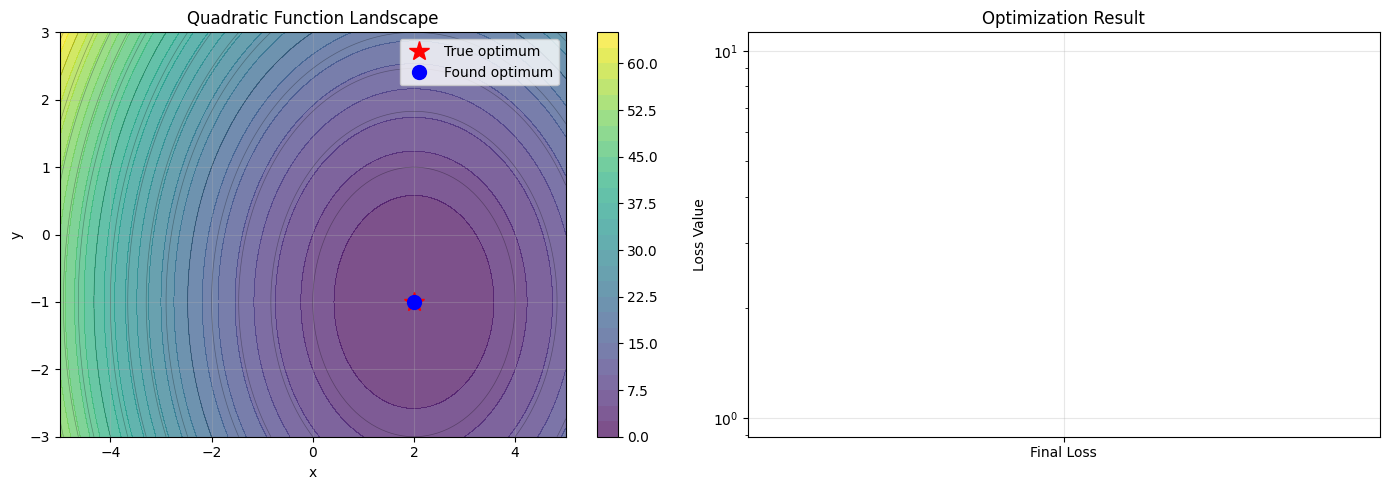

Let’s start with a simple example: optimizing a quadratic function with two scalar parameters.

# Define a simple quadratic loss function

def quadratic_loss(x, y):

"""

Simple quadratic function with known minimum at (2, -1).

Args:

x, y: Scalar parameters

Returns:

Scalar loss value

"""

return (x - 2.0)**2 + (y + 1.0)**2

# Define bounds for each parameter: (min, max)

bounds = [

(-5.0, 5.0), # bounds for x

(-3.0, 3.0), # bounds for y

]

# Create the optimizer

optimizer = bts.optim.ScipyOptimizer(

loss_fun=quadratic_loss,

bounds=bounds,

method='L-BFGS-B' # Limited-memory BFGS with bounds

)

print("Optimizer created successfully!")

print(f"Method: {optimizer.method}")

print(f"Bounds structure: {type(bounds).__name__}")

Optimizer created successfully!

Method: L-BFGS-B

Bounds structure: list

# Run the optimization

result = optimizer.minimize(n_iter=3) # Try 3 random starting points

print(f"\nOptimization completed!")

print(f"Success: {result.success}")

print(f"Message: {result.message}")

print(f"Optimal parameters: x={result.x[0]:.6f}, y={result.x[1]:.6f}")

print(f"True optimum: x=2.0, y=-1.0")

print(f"Final loss: {result.fun:.10f}")

print(f"Function evaluations: {result.nfev}")

print(f"Gradient evaluations: {result.njev}")

Optimization completed!

Success: True

Message: CONVERGENCE: NORM_OF_PROJECTED_GRADIENT_<=_PGTOL

Optimal parameters: x=2.000000, y=-1.000000

True optimum: x=2.0, y=-1.0

Final loss: 0.0000000000

Function evaluations: 4

Gradient evaluations: 4

# Visualize the optimization landscape and result

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(14, 5))

# Plot the function landscape

x_range = np.linspace(-5, 5, 100)

y_range = np.linspace(-3, 3, 100)

X, Y = np.meshgrid(x_range, y_range)

Z = (X - 2.0)**2 + (Y + 1.0)**2

contour = ax1.contourf(X, Y, Z, levels=30, cmap='viridis', alpha=0.7)

ax1.contour(X, Y, Z, levels=20, colors='black', alpha=0.3, linewidths=0.5)

plt.colorbar(contour, ax=ax1)

# Mark the true optimum and found optimum

ax1.plot(2.0, -1.0, 'r*', markersize=15, label='True optimum')

ax1.plot(result.x[0], result.x[1], 'bo', markersize=10, label='Found optimum')

ax1.set_xlabel('x')

ax1.set_ylabel('y')

ax1.set_title('Quadratic Function Landscape')

ax1.legend()

ax1.grid(True, alpha=0.3)

# Show convergence (we don't have iteration history, so show final result)

ax2.bar(['Final Loss'], [result.fun], color='blue', alpha=0.7)

ax2.set_ylabel('Loss Value')

ax2.set_title('Optimization Result')

ax2.set_yscale('log')

ax2.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

print(f"Distance from true optimum: {np.sqrt((result.x[0] - 2.0)**2 + (result.x[1] + 1.0)**2):.2e}")

C:\Users\adadu\AppData\Local\Temp\ipykernel_59268\1560779676.py:28: UserWarning: Data has no positive values, and therefore cannot be log-scaled.

ax2.set_yscale('log')

Distance from true optimum: 0.00e+00

Multi-dimensional Array Parameters#

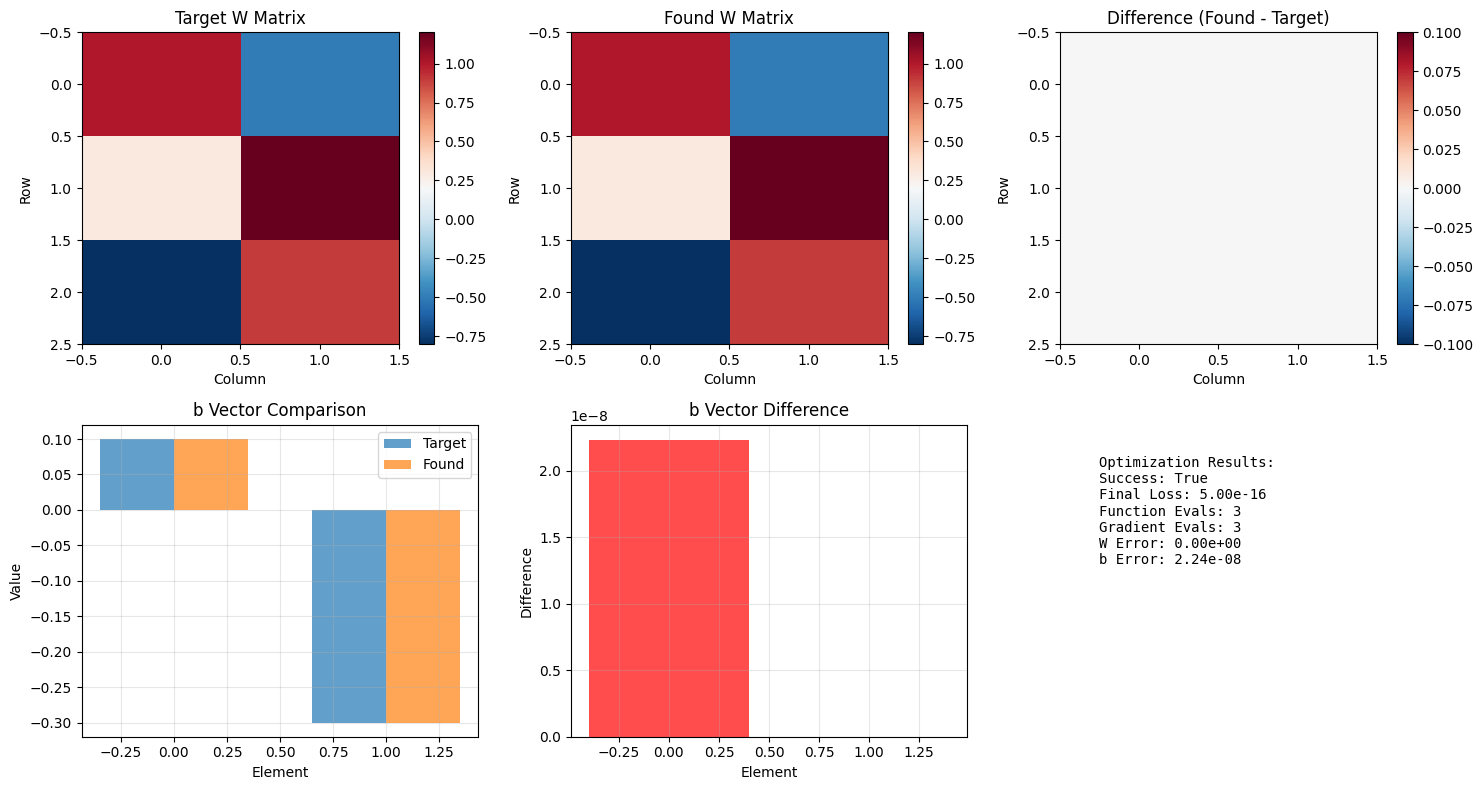

The ScipyOptimizer can handle multi-dimensional arrays as parameters. Let’s optimize a function that takes matrix parameters.

# Define a loss function with matrix parameters

def matrix_frobenius_loss(W, b):

"""

Find matrix W and vector b that minimize Frobenius norm from targets.

Args:

W: Matrix parameter of shape (3, 2)

b: Vector parameter of shape (2,)

Returns:

Scalar loss (Frobenius norm squared)

"""

W_target = jnp.array([[1.0, -0.5], [0.3, 1.2], [-0.8, 0.9]])

b_target = jnp.array([0.1, -0.3])

W_diff = W - W_target

b_diff = b - b_target

return jnp.sum(W_diff**2) + jnp.sum(b_diff**2)

# Define bounds for array parameters

bounds = [

(jnp.full((3, 2), -2.0), jnp.full((3, 2), 2.0)), # bounds for W (3x2 matrix)

(jnp.full(2, -1.0), jnp.full(2, 1.0)), # bounds for b (2D vector)

]

# Create optimizer

matrix_optimizer = bts.optim.ScipyOptimizer(

loss_fun=matrix_frobenius_loss,

bounds=bounds,

method='L-BFGS-B' # Good for smooth, bounded problems

)

print("Multi-dimensional optimizer created!")

print(f"W parameter shape: {bounds[0][0].shape}")

print(f"b parameter shape: {bounds[1][0].shape}")

Multi-dimensional optimizer created!

W parameter shape: (3, 2)

b parameter shape: (2,)

# Run optimization

matrix_result = matrix_optimizer.minimize(n_iter=5)

W_best, b_best = matrix_result.x

print(f"\nOptimization completed!")

print(f"Success: {matrix_result.success}")

print(f"Function evaluations: {matrix_result.nfev}")

print(f"\nOptimal W matrix:")

print(W_best)

print(f"\nOptimal b vector:")

print(b_best)

# Compare with targets

W_target = jnp.array([[1.0, -0.5], [0.3, 1.2], [-0.8, 0.9]])

b_target = jnp.array([0.1, -0.3])

print(f"\nTarget W matrix:")

print(W_target)

print(f"\nTarget b vector:")

print(b_target)

print(f"\nFinal loss: {matrix_result.fun:.10f}")

print(f"W error (Frobenius): {jnp.linalg.norm(W_best - W_target):.2e}")

print(f"b error (L2): {jnp.linalg.norm(b_best - b_target):.2e}")

Optimization completed!

Success: True

Function evaluations: 3

Optimal W matrix:

[[ 1. -0.5]

[ 0.3 1.2]

[-0.8 0.9]]

Optimal b vector:

[ 0.10000002 -0.3 ]

Target W matrix:

[[ 1. -0.5]

[ 0.3 1.2]

[-0.8 0.9]]

Target b vector:

[ 0.1 -0.3]

Final loss: 0.0000000000

W error (Frobenius): 0.00e+00

b error (L2): 2.24e-08

# Visualize the matrix optimization results

fig, axes = plt.subplots(2, 3, figsize=(15, 8))

# Plot W matrix: target, found, and difference

im1 = axes[0, 0].imshow(W_target, cmap='RdBu_r', aspect='auto')

axes[0, 0].set_title('Target W Matrix')

axes[0, 0].set_xlabel('Column')

axes[0, 0].set_ylabel('Row')

plt.colorbar(im1, ax=axes[0, 0])

im2 = axes[0, 1].imshow(W_best, cmap='RdBu_r', aspect='auto')

axes[0, 1].set_title('Found W Matrix')

axes[0, 1].set_xlabel('Column')

axes[0, 1].set_ylabel('Row')

plt.colorbar(im2, ax=axes[0, 1])

W_diff = W_best - W_target

im3 = axes[0, 2].imshow(W_diff, cmap='RdBu_r', aspect='auto')

axes[0, 2].set_title('Difference (Found - Target)')

axes[0, 2].set_xlabel('Column')

axes[0, 2].set_ylabel('Row')

plt.colorbar(im3, ax=axes[0, 2])

# Plot b vector: target, found, and difference

x_pos = np.arange(len(b_target))

width = 0.35

axes[1, 0].bar(x_pos - width/2, b_target, width, label='Target', alpha=0.7)

axes[1, 0].bar(x_pos + width/2, b_best, width, label='Found', alpha=0.7)

axes[1, 0].set_xlabel('Element')

axes[1, 0].set_ylabel('Value')

axes[1, 0].set_title('b Vector Comparison')

axes[1, 0].legend()

axes[1, 0].grid(True, alpha=0.3)

# Plot the difference in b

b_diff = b_best - b_target

axes[1, 1].bar(x_pos, b_diff, alpha=0.7, color='red')

axes[1, 1].set_xlabel('Element')

axes[1, 1].set_ylabel('Difference')

axes[1, 1].set_title('b Vector Difference')

axes[1, 1].grid(True, alpha=0.3)

# Plot optimization info

info_text = f"""Optimization Results:

Success: {matrix_result.success}

Final Loss: {matrix_result.fun:.2e}

Function Evals: {matrix_result.nfev}

Gradient Evals: {matrix_result.njev}

W Error: {jnp.linalg.norm(W_diff):.2e}

b Error: {jnp.linalg.norm(b_diff):.2e}"""

axes[1, 2].text(0.1, 0.9, info_text, transform=axes[1, 2].transAxes,

verticalalignment='top', fontsize=10, fontfamily='monospace')

axes[1, 2].set_xlim(0, 1)

axes[1, 2].set_ylim(0, 1)

axes[1, 2].axis('off')

plt.tight_layout()

plt.show()

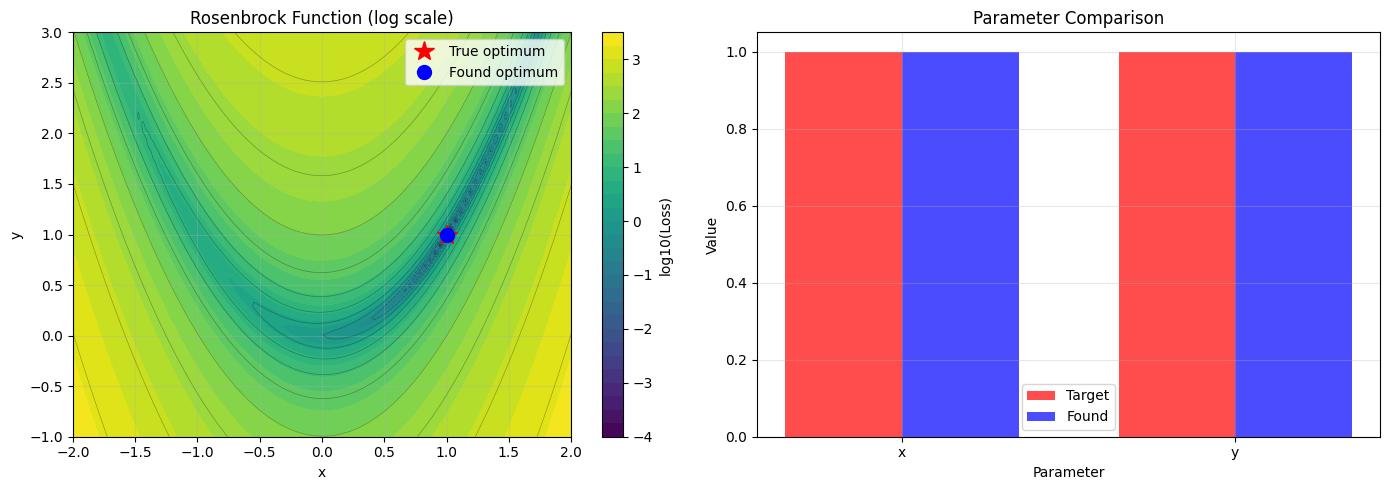

Named Parameters with Dictionary Bounds#

For better organization, especially with many parameters, you can use dictionary bounds to give meaningful names to your parameters.

# Define a loss function that accepts named parameters

def rosenbrock_loss(**params):

"""

The famous Rosenbrock function with named parameters.

Global minimum at x=1, y=1 with value 0.

Args:

**params: Dictionary with keys 'x' and 'y'

Returns:

Scalar loss value

"""

x, y = params['x'], params['y']

a, b = 1.0, 100.0

return (a - x)**2 + b * (y - x**2)**2

# Define named bounds

named_bounds = {

'x': (-2.0, 2.0),

'y': (-1.0, 3.0)

}

# Create optimizer with named parameters

named_optimizer = bts.optim.ScipyOptimizer(

loss_fun=rosenbrock_loss,

bounds=named_bounds,

method='L-BFGS-B'

)

print("Named parameter optimizer created!")

print(f"Parameters: {list(named_bounds.keys())}")

Named parameter optimizer created!

Parameters: ['x', 'y']

# Run optimization

named_result = named_optimizer.minimize(n_iter=5)

print(f"\nOptimization completed!")

print(f"Success: {named_result.success}")

print(f"Function evaluations: {named_result.nfev}")

print(f"Gradient evaluations: {named_result.njev}")

print(f"\nOptimal parameters:")

for param_name, value in named_result.x.items():

print(f" {param_name}: {value:.6f}")

print(f"\nTrue optimal values:")

print(f" x: 1.000000")

print(f" y: 1.000000")

print(f"\nFinal loss: {named_result.fun:.10f}")

print(f"Distance from optimum: {np.sqrt((named_result.x['x'] - 1.0)**2 + (named_result.x['y'] - 1.0)**2):.2e}")

Optimization completed!

Success: True

Function evaluations: 30

Gradient evaluations: 30

Optimal parameters:

x: 1.000000

y: 1.000000

True optimal values:

x: 1.000000

y: 1.000000

Final loss: 0.0000000000

Distance from optimum: 2.67e-07

# Visualize the Rosenbrock function and optimization result

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(14, 5))

# Plot the Rosenbrock function landscape

x_range = np.linspace(-2, 2, 100)

y_range = np.linspace(-1, 3, 100)

X, Y = np.meshgrid(x_range, y_range)

Z = (1 - X)**2 + 100 * (Y - X**2)**2

# Use log scale for better visualization

Z_log = np.log10(Z + 1e-10)

contour = ax1.contourf(X, Y, Z_log, levels=30, cmap='viridis')

ax1.contour(X, Y, Z_log, levels=20, colors='black', alpha=0.3, linewidths=0.5)

plt.colorbar(contour, ax=ax1, label='log10(Loss)')

# Mark the true optimum and found optimum

ax1.plot(1.0, 1.0, 'r*', markersize=15, label='True optimum')

ax1.plot(named_result.x['x'], named_result.x['y'], 'bo', markersize=10, label='Found optimum')

ax1.set_xlabel('x')

ax1.set_ylabel('y')

ax1.set_title('Rosenbrock Function (log scale)')

ax1.legend()

ax1.grid(True, alpha=0.3)

# Plot parameter values

param_names = list(named_result.x.keys())

param_values = [named_result.x[name] for name in param_names]

target_values = [1.0, 1.0]

x_pos = np.arange(len(param_names))

width = 0.35

ax2.bar(x_pos - width/2, target_values, width, label='Target', alpha=0.7, color='red')

ax2.bar(x_pos + width/2, param_values, width, label='Found', alpha=0.7, color='blue')

ax2.set_xlabel('Parameter')

ax2.set_ylabel('Value')

ax2.set_title('Parameter Comparison')

ax2.set_xticks(x_pos)

ax2.set_xticklabels(param_names)

ax2.legend()

ax2.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

Working with BrainUnit Quantities#

The ScipyOptimizer seamlessly integrates with BrainUnit quantities, allowing you to optimize parameters with physical units.

# Define a loss function for neuron model parameters with units

def neuron_model_loss(tau_m, V_th, V_reset, I_ext):

"""

Loss function for fitting a neuron model to target parameters.

Args:

tau_m: Membrane time constant (scalar)

V_th: Threshold voltage (scalar)

V_reset: Reset voltage (scalar)

I_ext: External current (scalar)

Returns:

Scalar loss representing deviation from target behavior

"""

# Target values (without units - optimizer handles unit conversion)

tau_target = 20.0 # ms

V_th_target = -50.0 # mV

V_reset_target = -70.0 # mV

I_target = 100.0 # pA

# Compute normalized squared differences

tau_loss = ((tau_m - tau_target) / 10.0)**2

V_th_loss = ((V_th - V_th_target) / 10.0)**2

V_reset_loss = ((V_reset - V_reset_target) / 10.0)**2

I_loss = ((I_ext - I_target) / 50.0)**2

return tau_loss + V_th_loss + V_reset_loss + I_loss

# Define bounds with units

unit_bounds = {

'tau_m': (5.0 * u.ms, 50.0 * u.ms),

'V_th': (-80.0 * u.mV, -30.0 * u.mV),

'V_reset': (-90.0 * u.mV, -60.0 * u.mV),

'I_ext': (10.0 * u.pA, 200.0 * u.pA)

}

# Create optimizer

unit_optimizer = bts.optim.ScipyOptimizer(

loss_fun=neuron_model_loss,

bounds=unit_bounds,

method='L-BFGS-B'

)

print("Neuron parameter optimizer with units created!")

for name, (low, high) in unit_bounds.items():

print(f" {name}: {low} to {high}")

Neuron parameter optimizer with units created!

tau_m: 5.0 * msecond to 50.0 * msecond

V_th: -80.0 * mvolt to -30.0 * mvolt

V_reset: -90.0 * mvolt to -60.0 * mvolt

I_ext: 10.0 * pamp to 200.0 * pamp

# Run optimization with units

unit_result = unit_optimizer.minimize(n_iter=3)

print(f"\nOptimization completed!")

print(f"Success: {unit_result.success}")

print(f"Function evaluations: {unit_result.nfev}")

print(f"\nOptimal neuron parameters:")

for param_name, value in unit_result.x.items():

print(f" {param_name}: {value:.6f}")

print(f"\nTarget parameters:")

print(f" tau_m: 20.0")

print(f" V_th: -50.0")

print(f" V_reset: -70.0")

print(f" I_ext: 100.0")

print(f"\nFinal loss: {unit_result.fun:.10f}")

# Note: The optimizer works with dimensionless values internally

# but maintains the parameter structure

Optimization completed!

Success: True

Function evaluations: 9

Optimal neuron parameters:

I_ext: 100.000000

V_reset: -70.000000

V_th: -50.000000

tau_m: 20.000000

Target parameters:

tau_m: 20.0

V_th: -50.0

V_reset: -70.0

I_ext: 100.0

Final loss: 0.0000000000

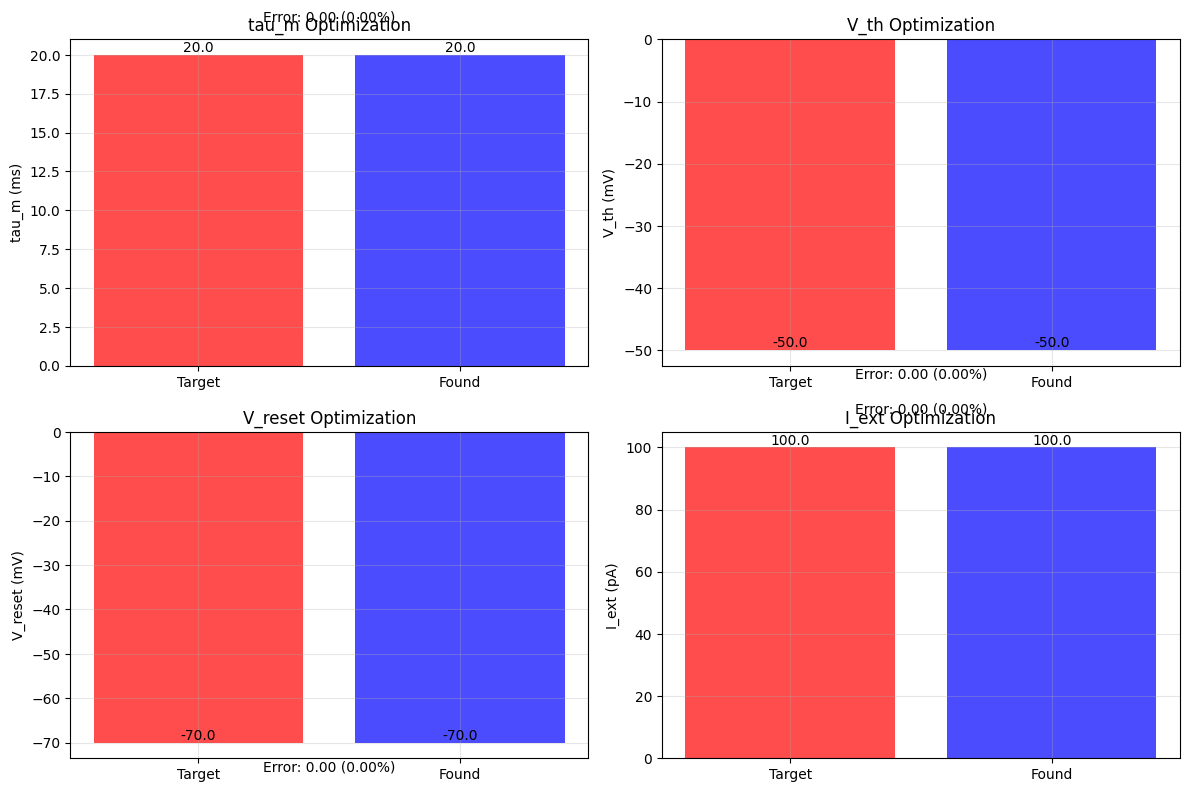

# Visualize neuron parameter optimization results

fig, axes = plt.subplots(2, 2, figsize=(12, 8))

axes = axes.flatten()

# Define target values and units for visualization

targets = {

'tau_m': (20.0, 'ms'),

'V_th': (-50.0, 'mV'),

'V_reset': (-70.0, 'mV'),

'I_ext': (100.0, 'pA')

}

for i, (param_name, (target_val, unit)) in enumerate(targets.items()):

found_val = unit_result.x[param_name]

# Plot comparison

axes[i].bar(['Target', 'Found'], [target_val, found_val],

color=['red', 'blue'], alpha=0.7)

axes[i].set_ylabel(f'{param_name} ({unit})')

axes[i].set_title(f'{param_name} Optimization')

axes[i].grid(True, alpha=0.3)

# Add value labels on bars

axes[i].text(0, target_val, f'{target_val:.1f}', ha='center', va='bottom')

axes[i].text(1, found_val, f'{found_val:.1f}', ha='center', va='bottom')

# Add error information

error = abs(found_val - target_val)

rel_error = error / abs(target_val) * 100

axes[i].text(0.5, max(target_val, found_val) * 1.1,

f'Error: {error:.2f} ({rel_error:.2f}%)',

ha='center', va='bottom', fontsize=10)

plt.tight_layout()

plt.show()

print("\nParameter Errors:")

for param_name, (target_val, unit) in targets.items():

found_val = unit_result.x[param_name]

error = abs(found_val - target_val)

rel_error = error / abs(target_val) * 100

print(f" {param_name}: {error:.3f} {unit} ({rel_error:.2f}%)")

Parameter Errors:

tau_m: 0.000 ms (0.00%)

V_th: 0.000 mV (0.00%)

V_reset: 0.000 mV (0.00%)

I_ext: 0.000 pA (0.00%)

Different SciPy Methods#

SciPy provides many optimization algorithms. Let’s compare several of them on the same problem.

# Define a more challenging test function

def beale_function(x, y):

"""

Beale function - a challenging optimization benchmark.

Global minimum at (3, 0.5) with value 0.

"""

return ((1.5 - x + x*y)**2 +

(2.25 - x + x*y**2)**2 +

(2.625 - x + x*y**3)**2)

bounds = [(-4.5, 4.5), (-4.5, 4.5)]

# Test different SciPy methods

methods = [

'L-BFGS-B', # Limited memory BFGS with bounds

# 'TNC', # Truncated Newton with bounds

'SLSQP', # Sequential Least Squares Programming

'Powell', # Powell's method (derivative-free but included for comparison)

]

results = {}

print("Testing different SciPy optimization methods...\n")

for method in methods:

print(f"Testing {method}...")

optimizer = bts.optim.ScipyOptimizer(

loss_fun=beale_function,

bounds=bounds,

method=method

)

result = optimizer.minimize(n_iter=3)

results[method] = {

'result': result,

'success': result.success,

'final_loss': result.fun,

'nfev': result.nfev,

'njev': getattr(result, 'njev', 0),

'params': result.x

}

print(f" Success: {result.success}")

print(f" Final loss: {result.fun:.8f}")

print(f" Parameters: ({result.x[0]:.4f}, {result.x[1]:.4f})")

print(f" Function evaluations: {result.nfev}")

if hasattr(result, 'njev'):

print(f" Gradient evaluations: {result.njev}")

print()

print("Method comparison completed!")

print(f"\nTrue optimum: (3.0, 0.5) with loss = 0.0")

Testing different SciPy optimization methods...

Testing L-BFGS-B...

Success: True

Final loss: 0.00000000

Parameters: (3.0000, 0.5000)

Function evaluations: 21

Gradient evaluations: 21

Testing SLSQP...

Success: True

Final loss: 0.00000011

Parameters: (2.9992, 0.4998)

Function evaluations: 42

Gradient evaluations: 33

Testing Powell...

D:\codes\projects\braintools\braintools\optim\_scipy_optimizer.py:286: RuntimeWarning: Method Powell does not use gradient information (jac).

results = minimize(

Success: True

Final loss: 0.00000000

Parameters: (3.0000, 0.5000)

Function evaluations: 483

Method comparison completed!

True optimum: (3.0, 0.5) with loss = 0.0

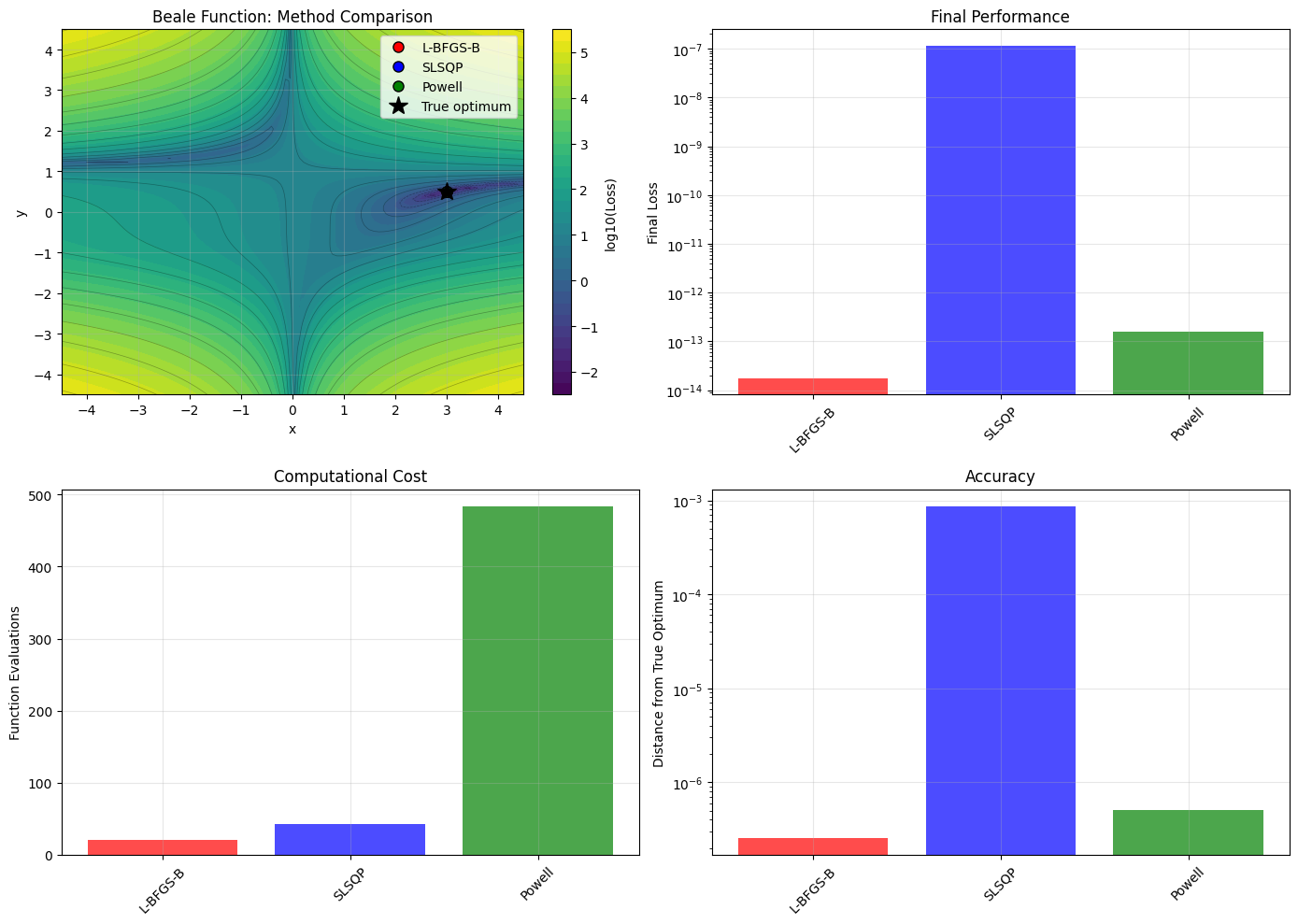

# Visualize method comparison

fig, axes = plt.subplots(2, 2, figsize=(14, 10))

# Plot the Beale function landscape

x_range = np.linspace(-4.5, 4.5, 100)

y_range = np.linspace(-4.5, 4.5, 100)

X, Y = np.meshgrid(x_range, y_range)

Z = ((1.5 - X + X*Y)**2 +

(2.25 - X + X*Y**2)**2 +

(2.625 - X + X*Y**3)**2)

# Use log scale for better visualization

Z_log = np.log10(Z + 1e-10)

contour = axes[0, 0].contourf(X, Y, Z_log, levels=30, cmap='viridis')

axes[0, 0].contour(X, Y, Z_log, levels=20, colors='black', alpha=0.3, linewidths=0.5)

plt.colorbar(contour, ax=axes[0, 0], label='log10(Loss)')

# Plot results from different methods

colors = ['red', 'blue', 'green', 'orange']

for i, (method, result_data) in enumerate(results.items()):

x_opt, y_opt = result_data['params']

axes[0, 0].plot(x_opt, y_opt, 'o', color=colors[i], markersize=8,

label=f'{method}', markeredgecolor='black')

# Mark true optimum

axes[0, 0].plot(3.0, 0.5, '*', color='black', markersize=15, label='True optimum')

axes[0, 0].set_xlabel('x')

axes[0, 0].set_ylabel('y')

axes[0, 0].set_title('Beale Function: Method Comparison')

axes[0, 0].legend()

axes[0, 0].grid(True, alpha=0.3)

# Plot final losses

method_names = list(results.keys())

final_losses = [results[m]['final_loss'] for m in method_names]

bars = axes[0, 1].bar(method_names, final_losses, color=colors[:len(method_names)], alpha=0.7)

axes[0, 1].set_yscale('log')

axes[0, 1].set_ylabel('Final Loss')

axes[0, 1].set_title('Final Performance')

axes[0, 1].tick_params(axis='x', rotation=45)

axes[0, 1].grid(True, alpha=0.3)

# Plot function evaluations

nfevs = [results[m]['nfev'] for m in method_names]

axes[1, 0].bar(method_names, nfevs, color=colors[:len(method_names)], alpha=0.7)

axes[1, 0].set_ylabel('Function Evaluations')

axes[1, 0].set_title('Computational Cost')

axes[1, 0].tick_params(axis='x', rotation=45)

axes[1, 0].grid(True, alpha=0.3)

# Plot success/distance from optimum

distances = []

for method in method_names:

x_opt, y_opt = results[method]['params']

dist = np.sqrt((x_opt - 3.0)**2 + (y_opt - 0.5)**2)

distances.append(dist)

bars = axes[1, 1].bar(method_names, distances, color=colors[:len(method_names)], alpha=0.7)

axes[1, 1].set_yscale('log')

axes[1, 1].set_ylabel('Distance from True Optimum')

axes[1, 1].set_title('Accuracy')

axes[1, 1].tick_params(axis='x', rotation=45)

axes[1, 1].grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

# Print summary

print("\nMethod Performance Summary:")

print("Method\t\tSuccess\tFinal Loss\tFunc Evals\tDistance")

print("-" * 65)

for i, method in enumerate(method_names):

data = results[method]

print(f"{method:12s}\t{data['success']}\t{data['final_loss']:.2e}\t{data['nfev']:4d}\t\t{distances[i]:.2e}")

Method Performance Summary:

Method Success Final Loss Func Evals Distance

-----------------------------------------------------------------

L-BFGS-B True 1.78e-14 21 2.55e-07

SLSQP True 1.15e-07 42 8.72e-04

Powell True 1.60e-13 483 5.09e-07

Neural Network Parameter Optimization#

Let’s demonstrate a practical application: optimizing parameters of a simple neural network.

# Generate synthetic regression data

np.random.seed(42)

n_samples = 200

n_features = 3

# Create synthetic data with known pattern

X = np.random.randn(n_samples, n_features)

# True relationship: y = 2*x1 - 1.5*x2 + 0.8*x3 + noise

true_weights = np.array([2.0, -1.5, 0.8])

y = X @ true_weights + 0.1 * np.random.randn(n_samples)

# Split into train/test

split = int(0.8 * n_samples)

X_train, X_test = jnp.array(X[:split]), jnp.array(X[split:])

y_train, y_test = jnp.array(y[:split]), jnp.array(y[split:])

print(f"Training set: {X_train.shape[0]} samples")

print(f"Test set: {X_test.shape[0]} samples")

print(f"True weights: {true_weights}")

Training set: 160 samples

Test set: 40 samples

True weights: [ 2. -1.5 0.8]

# Define a simple neural network loss function

def neural_network_loss(W1, b1, W2, b2):

"""

Loss function for a simple 2-layer neural network.

Args:

W1: First layer weights, shape (n_features, hidden_size)

b1: First layer bias, shape (hidden_size,)

W2: Second layer weights, shape (hidden_size, 1)

b2: Second layer bias, shape (1,)

Returns:

Mean squared error on training set

"""

# Forward pass

h = jax.nn.relu(X_train @ W1 + b1) # Hidden layer with ReLU

y_pred = h @ W2 + b2 # Output layer

# Mean squared error

mse = jnp.mean((y_pred.flatten() - y_train)**2)

# Add small L2 regularization

l2_reg = 0.01 * (jnp.sum(W1**2) + jnp.sum(W2**2))

return mse + l2_reg

# Define bounds for network parameters

hidden_size = 5

network_bounds = {

'W1': (jnp.full((n_features, hidden_size), -2.0), jnp.full((n_features, hidden_size), 2.0)),

'b1': (jnp.full(hidden_size, -1.0), jnp.full(hidden_size, 1.0)),

'W2': (jnp.full((hidden_size, 1), -2.0), jnp.full((hidden_size, 1), 2.0)),

'b2': (jnp.full(1, -1.0), jnp.full(1, 1.0))

}

print(f"Neural network architecture: {n_features} -> {hidden_size} -> 1")

print(f"Total parameters: {n_features * hidden_size + hidden_size + hidden_size * 1 + 1}")

Neural network architecture: 3 -> 5 -> 1

Total parameters: 26

# Create and run neural network optimizer

nn_optimizer = bts.optim.ScipyOptimizer(

loss_fun=neural_network_loss,

bounds=network_bounds,

method='L-BFGS-B',

options={'maxiter': 1000} # Allow more iterations for neural network

)

print("Optimizing neural network parameters...")

print("(This may take a moment)\n")

nn_result = nn_optimizer.minimize(n_iter=3)

print(f"Optimization completed!")

print(f"Success: {nn_result.success}")

print(f"Function evaluations: {nn_result.nfev}")

print(f"Gradient evaluations: {nn_result.njev}")

print(f"Final training loss: {nn_result.fun:.6f}")

Optimizing neural network parameters...

(This may take a moment)

Optimization completed!

Success: True

Function evaluations: 196

Gradient evaluations: 196

Final training loss: 0.095723

# Evaluate the optimized network

def evaluate_network(W1, b1, W2, b2, X, y):

"""Evaluate network performance on given data."""

h = jax.nn.relu(X @ W1 + b1)

y_pred = h @ W2 + b2

mse = jnp.mean((y_pred.flatten() - y)**2)

return y_pred.flatten(), mse

# Get optimized parameters

W1_opt = nn_result.x['W1']

b1_opt = nn_result.x['b1']

W2_opt = nn_result.x['W2']

b2_opt = nn_result.x['b2']

# Evaluate on train and test sets

y_train_pred, train_mse = evaluate_network(W1_opt, b1_opt, W2_opt, b2_opt, X_train, y_train)

y_test_pred, test_mse = evaluate_network(W1_opt, b1_opt, W2_opt, b2_opt, X_test, y_test)

print(f"\nNetwork Performance:")

print(f"Training MSE: {train_mse:.6f}")

print(f"Test MSE: {test_mse:.6f}")

# Compare with linear regression baseline

linear_weights = jnp.linalg.lstsq(X_train, y_train, rcond=None)[0]

y_test_linear = X_test @ linear_weights

linear_mse = jnp.mean((y_test_linear - y_test)**2)

print(f"Linear regression MSE: {linear_mse:.6f}")

print(f"\nTrue weights: {true_weights}")

print(f"Linear regression weights: {linear_weights}")

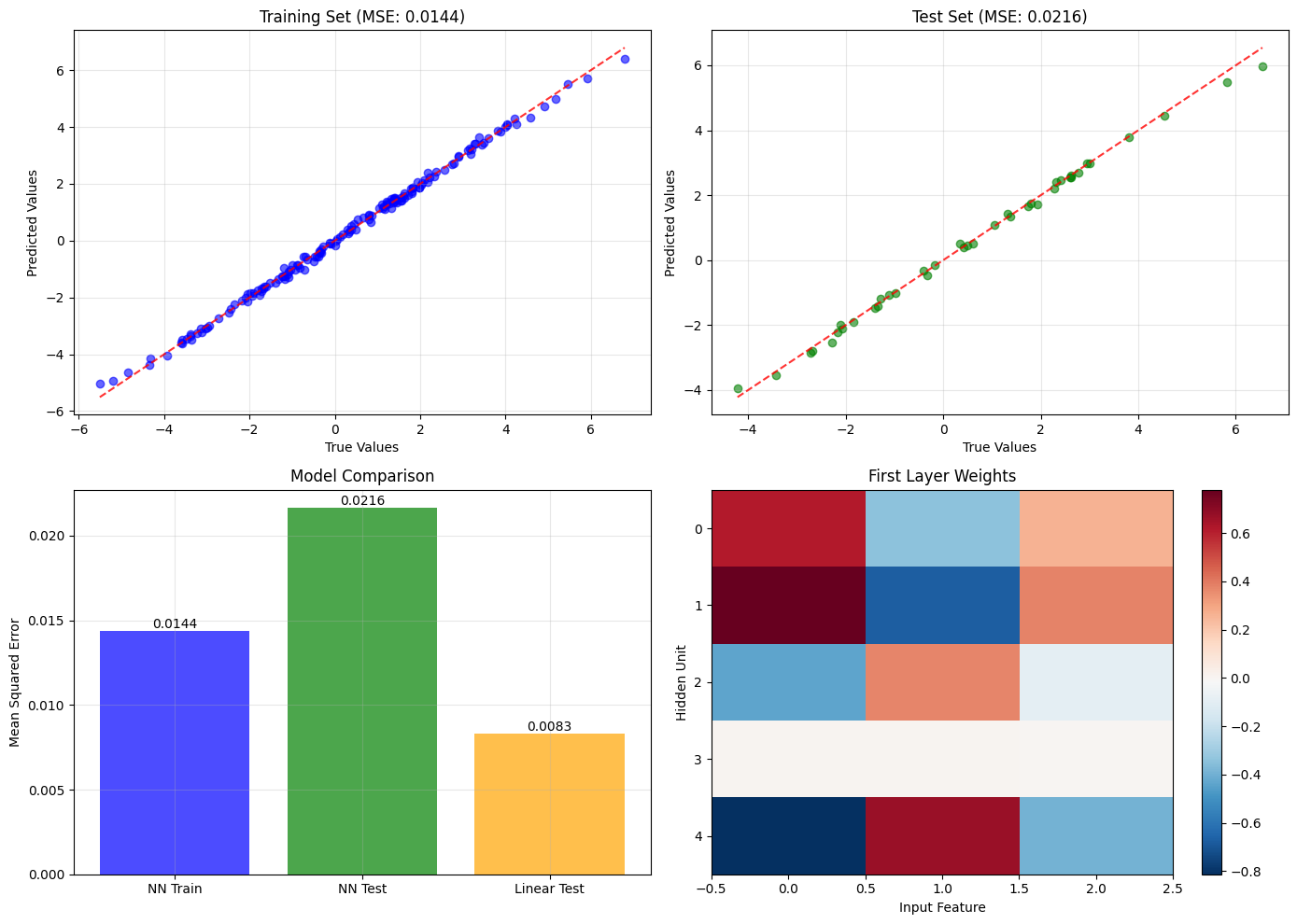

Network Performance:

Training MSE: 0.014361

Test MSE: 0.021628

Linear regression MSE: 0.008314

True weights: [ 2. -1.5 0.8]

Linear regression weights: [ 1.9943104 -1.4900746 0.81011224]

# Visualize neural network results

fig, axes = plt.subplots(2, 2, figsize=(14, 10))

# Plot predictions vs true values for training set

axes[0, 0].scatter(y_train, y_train_pred, alpha=0.6, color='blue')

min_val, max_val = min(jnp.min(y_train), jnp.min(y_train_pred)), max(jnp.max(y_train), jnp.max(y_train_pred))

axes[0, 0].plot([min_val, max_val], [min_val, max_val], 'r--', alpha=0.8)

axes[0, 0].set_xlabel('True Values')

axes[0, 0].set_ylabel('Predicted Values')

axes[0, 0].set_title(f'Training Set (MSE: {train_mse:.4f})')

axes[0, 0].grid(True, alpha=0.3)

# Plot predictions vs true values for test set

axes[0, 1].scatter(y_test, y_test_pred, alpha=0.6, color='green')

min_val, max_val = min(jnp.min(y_test), jnp.min(y_test_pred)), max(jnp.max(y_test), jnp.max(y_test_pred))

axes[0, 1].plot([min_val, max_val], [min_val, max_val], 'r--', alpha=0.8)

axes[0, 1].set_xlabel('True Values')

axes[0, 1].set_ylabel('Predicted Values')

axes[0, 1].set_title(f'Test Set (MSE: {test_mse:.4f})')

axes[0, 1].grid(True, alpha=0.3)

# Compare MSE values

mse_values = [train_mse, test_mse, linear_mse]

mse_labels = ['NN Train', 'NN Test', 'Linear Test']

colors = ['blue', 'green', 'orange']

bars = axes[1, 0].bar(mse_labels, mse_values, color=colors, alpha=0.7)

axes[1, 0].set_ylabel('Mean Squared Error')

axes[1, 0].set_title('Model Comparison')

axes[1, 0].grid(True, alpha=0.3)

# Add value labels on bars

for bar, value in zip(bars, mse_values):

axes[1, 0].text(bar.get_x() + bar.get_width()/2, bar.get_height(),

f'{value:.4f}', ha='center', va='bottom')

# Plot weight comparison (first layer weights)

im = axes[1, 1].imshow(W1_opt.T, cmap='RdBu_r', aspect='auto')

axes[1, 1].set_xlabel('Input Feature')

axes[1, 1].set_ylabel('Hidden Unit')

axes[1, 1].set_title('First Layer Weights')

plt.colorbar(im, ax=axes[1, 1])

plt.tight_layout()

plt.show()

print(f"\nNetwork architecture summary:")

print(f"W1 shape: {W1_opt.shape}, range: [{jnp.min(W1_opt):.3f}, {jnp.max(W1_opt):.3f}]")

print(f"b1 shape: {b1_opt.shape}, range: [{jnp.min(b1_opt):.3f}, {jnp.max(b1_opt):.3f}]")

print(f"W2 shape: {W2_opt.shape}, range: [{jnp.min(W2_opt):.3f}, {jnp.max(W2_opt):.3f}]")

print(f"b2 shape: {b2_opt.shape}, value: {b2_opt[0]:.3f}")

Network architecture summary:

W1 shape: (3, 5), range: [-0.813, 0.779]

b1 shape: (5,), range: [-0.456, 1.000]

W2 shape: (5, 1), range: [-1.126, 1.165]

b2 shape: (1,), value: 0.171

Advanced Features: Constraints and Options#

The ScipyOptimizer supports advanced features like constraints and custom options.

# Example with constraints: optimize a portfolio with constraints

def portfolio_loss(weights):

"""

Portfolio optimization: minimize risk while maintaining expected return.

Args:

weights: Portfolio weights, shape (n_assets,)

Returns:

Portfolio variance (risk measure)

"""

# Synthetic covariance matrix (risk model)

cov_matrix = jnp.array([

[0.04, 0.01, 0.005],

[0.01, 0.09, 0.02],

[0.005, 0.02, 0.16]

])

# Portfolio variance

portfolio_var = weights.T @ cov_matrix @ weights

return portfolio_var

# Define constraints

def constraint_sum_to_one(weights):

"""Constraint: weights must sum to 1."""

return jnp.sum(weights) - 1.0

def constraint_min_return(weights):

"""Constraint: minimum expected return."""

expected_returns = jnp.array([0.08, 0.12, 0.15]) # 8%, 12%, 15%

portfolio_return = weights.T @ expected_returns

return portfolio_return - 0.10 # At least 10% return

# Convert constraints to scipy format

constraints = [

{'type': 'eq', 'fun': lambda w: float(constraint_sum_to_one(jnp.array(w)))},

{'type': 'ineq', 'fun': lambda w: float(constraint_min_return(jnp.array(w)))}

]

# Bounds: each weight between 0 and 1

n_assets = 3

portfolio_bounds = [(jnp.zeros(n_assets), jnp.ones(n_assets))]

# Create constrained optimizer

portfolio_optimizer = bts.optim.ScipyOptimizer(

loss_fun=portfolio_loss,

bounds=portfolio_bounds,

method='SLSQP', # Good for constrained optimization

constraints=constraints,

options={'ftol': 1e-9, 'disp': True}

)

print("Portfolio optimization with constraints:")

print("- Weights must sum to 1 (budget constraint)")

print("- Expected return >= 10%")

print("- Each weight between 0 and 1 (long-only)")

print()

portfolio_result = portfolio_optimizer.minimize(n_iter=3)

print(f"\nOptimization completed!")

print(f"Success: {portfolio_result.success}")

print(f"Message: {portfolio_result.message}")

optimal_weights = portfolio_result.x[0]

print(f"\nOptimal portfolio weights:")

asset_names = ['Asset A', 'Asset B', 'Asset C']

for i, (name, weight) in enumerate(zip(asset_names, optimal_weights)):

print(f" {name}: {weight:.4f} ({weight*100:.1f}%)")

# Verify constraints

weight_sum = jnp.sum(optimal_weights)

expected_returns = jnp.array([0.08, 0.12, 0.15])

portfolio_return = optimal_weights.T @ expected_returns

portfolio_risk = jnp.sqrt(portfolio_result.fun)

print(f"\nPortfolio metrics:")

print(f" Weight sum: {weight_sum:.6f} (should be 1.0)")

print(f" Expected return: {portfolio_return:.4f} ({portfolio_return*100:.1f}%)")

print(f" Risk (volatility): {portfolio_risk:.4f} ({portfolio_risk*100:.1f}%)")

print(f" Variance: {portfolio_result.fun:.6f}")

Portfolio optimization with constraints:

- Weights must sum to 1 (budget constraint)

- Expected return >= 10%

- Each weight between 0 and 1 (long-only)

Singular matrix C in LSQ subproblem (Exit mode 6)

Current function value: 0.1654115915298462

Iterations: 1

Function evaluations: 1

Gradient evaluations: 1

Singular matrix C in LSQ subproblem (Exit mode 6)

Current function value: 0.07909038662910461

Iterations: 1

Function evaluations: 1

Gradient evaluations: 1

Singular matrix C in LSQ subproblem (Exit mode 6)

Current function value: 0.10067348182201385

Iterations: 1

Function evaluations: 1

Gradient evaluations: 1

Optimization completed!

Success: False

Message: Singular matrix C in LSQ subproblem

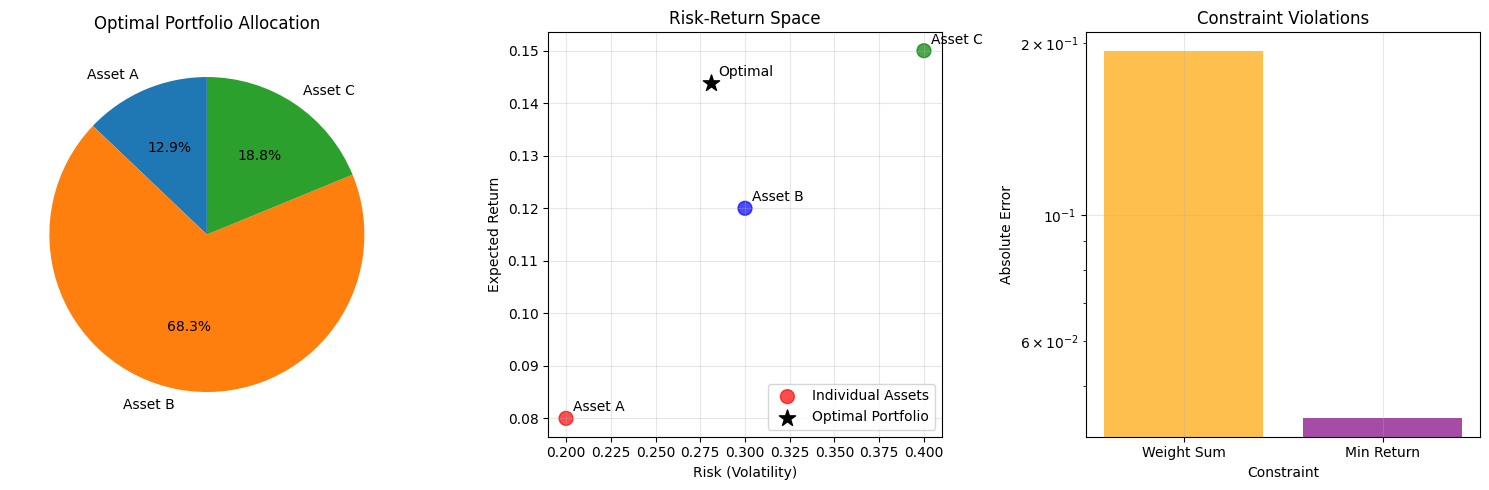

Optimal portfolio weights:

Asset A: 0.1539 (15.4%)

Asset B: 0.8158 (81.6%)

Asset C: 0.2244 (22.4%)

Portfolio metrics:

Weight sum: 1.194170 (should be 1.0)

Expected return: 0.1439 (14.4%)

Risk (volatility): 0.2812 (28.1%)

Variance: 0.079090

# Visualize portfolio optimization results

fig, axes = plt.subplots(1, 3, figsize=(15, 5))

# Plot portfolio weights

axes[0].pie(optimal_weights, labels=asset_names, autopct='%1.1f%%', startangle=90)

axes[0].set_title('Optimal Portfolio Allocation')

# Plot risk-return characteristics

asset_returns = jnp.array([0.08, 0.12, 0.15])

asset_risks = jnp.sqrt(jnp.diag(jnp.array([

[0.04, 0.01, 0.005],

[0.01, 0.09, 0.02],

[0.005, 0.02, 0.16]

])))

# Plot individual assets

axes[1].scatter(asset_risks, asset_returns, c=['red', 'blue', 'green'],

s=100, alpha=0.7, label='Individual Assets')

for i, name in enumerate(asset_names):

axes[1].annotate(name, (asset_risks[i], asset_returns[i]),

xytext=(5, 5), textcoords='offset points')

# Plot optimal portfolio

axes[1].scatter(portfolio_risk, portfolio_return, c='black',

s=150, marker='*', label='Optimal Portfolio')

axes[1].annotate('Optimal', (portfolio_risk, portfolio_return),

xytext=(5, 5), textcoords='offset points')

axes[1].set_xlabel('Risk (Volatility)')

axes[1].set_ylabel('Expected Return')

axes[1].set_title('Risk-Return Space')

axes[1].legend()

axes[1].grid(True, alpha=0.3)

# Plot constraint satisfaction

constraint_names = ['Weight Sum', 'Min Return']

constraint_values = [weight_sum, portfolio_return]

constraint_targets = [1.0, 0.10]

constraint_errors = [abs(cv - ct) for cv, ct in zip(constraint_values, constraint_targets)]

x_pos = np.arange(len(constraint_names))

axes[2].bar(x_pos, constraint_errors, alpha=0.7, color=['orange', 'purple'])

axes[2].set_xlabel('Constraint')

axes[2].set_ylabel('Absolute Error')

axes[2].set_title('Constraint Violations')

axes[2].set_xticks(x_pos)

axes[2].set_xticklabels(constraint_names)

axes[2].set_yscale('log')

axes[2].grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

Comparison with Derivative-Free Methods#

Let’s compare the ScipyOptimizer with the derivative-free NevergradOptimizer on the same problem.

# Define a test function for comparison

def comparison_function(x, y):

"""A smooth function suitable for gradient-based optimization."""

return (x - 1.5)**2 + 2*(y + 0.5)**2 + 0.1*jnp.sin(10*x)*jnp.cos(10*y)

bounds = [(-3.0, 3.0), (-2.0, 2.0)]

# Test ScipyOptimizer

print("Testing ScipyOptimizer (gradient-based)...")

scipy_opt = bts.optim.ScipyOptimizer(

loss_fun=comparison_function,

bounds=bounds,

method='L-BFGS-B'

)

import time

start_time = time.time()

scipy_result = scipy_opt.minimize(n_iter=3)

scipy_time = time.time() - start_time

print(f" Success: {scipy_result.success}")

print(f" Final loss: {scipy_result.fun:.8f}")

print(f" Parameters: ({scipy_result.x[0]:.6f}, {scipy_result.x[1]:.6f})")

print(f" Function evaluations: {scipy_result.nfev}")

print(f" Time: {scipy_time:.4f} seconds\n")

# Test NevergradOptimizer (if available)

try:

print("Testing NevergradOptimizer (derivative-free)...")

# Define batched version for Nevergrad

def batched_comparison_function(x, y):

return (x - 1.5)**2 + 2*(y + 0.5)**2 + 0.1*jnp.sin(10*x)*jnp.cos(10*y)

nevergrad_opt = bts.optim.NevergradOptimizer(

batched_loss_fun=batched_comparison_function,

bounds=bounds,

n_sample=10,

method='L-BFGS-B' # Actually uses scipy internally for this method

)

start_time = time.time()

nevergrad_result = nevergrad_opt.minimize(n_iter=20, verbose=False)

nevergrad_time = time.time() - start_time

print(f" Final loss: {comparison_function(nevergrad_result[0], nevergrad_result[1]):.8f}")

print(f" Parameters: ({nevergrad_result[0]:.6f}, {nevergrad_result[1]:.6f})")

print(f" Function evaluations: {len(nevergrad_opt.errors)}")

print(f" Time: {nevergrad_time:.4f} seconds\n")

nevergrad_available = True

except Exception as e:

print(f" NevergradOptimizer not available: {e}\n")

nevergrad_available = False

print(f"True optimum: (1.5, -0.5) with loss ≈ 0.0")

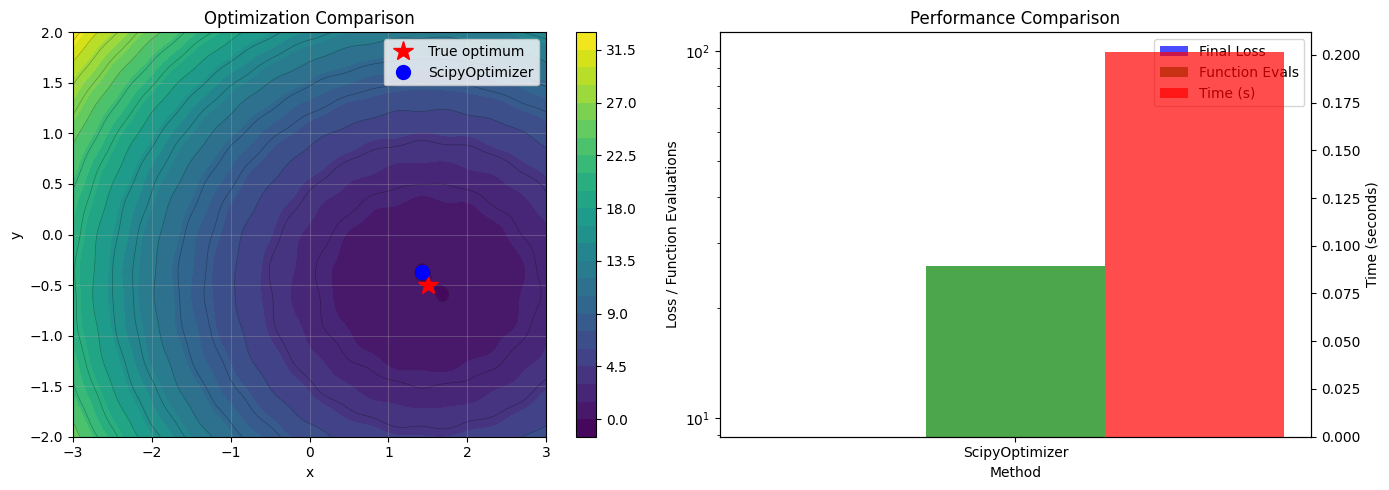

Testing ScipyOptimizer (gradient-based)...

Success: True

Final loss: -0.04498873

Parameters: (1.430242, -0.369797)

Function evaluations: 26

Time: 0.2017 seconds

Testing NevergradOptimizer (derivative-free)...

NevergradOptimizer not available: 'L-BFGS-B'

True optimum: (1.5, -0.5) with loss ≈ 0.0

# Visualize the comparison

fig, axes = plt.subplots(1, 2, figsize=(14, 5))

# Plot the function landscape

x_range = np.linspace(-3, 3, 200)

y_range = np.linspace(-2, 2, 200)

X, Y = np.meshgrid(x_range, y_range)

Z = (X - 1.5)**2 + 2*(Y + 0.5)**2 + 0.1*np.sin(10*X)*np.cos(10*Y)

contour = axes[0].contourf(X, Y, Z, levels=30, cmap='viridis')

axes[0].contour(X, Y, Z, levels=20, colors='black', alpha=0.3, linewidths=0.5)

plt.colorbar(contour, ax=axes[0])

# Mark results

axes[0].plot(1.5, -0.5, 'r*', markersize=15, label='True optimum')

axes[0].plot(scipy_result.x[0], scipy_result.x[1], 'bo', markersize=10, label='ScipyOptimizer')

if nevergrad_available:

axes[0].plot(nevergrad_result[0], nevergrad_result[1], 'gs', markersize=10, label='NevergradOptimizer')

axes[0].set_xlabel('x')

axes[0].set_ylabel('y')

axes[0].set_title('Optimization Comparison')

axes[0].legend()

axes[0].grid(True, alpha=0.3)

# Compare performance metrics

if nevergrad_available:

methods = ['ScipyOptimizer', 'NevergradOptimizer']

final_losses = [scipy_result.fun, comparison_function(nevergrad_result[0], nevergrad_result[1])]

func_evals = [scipy_result.nfev, len(nevergrad_opt.errors)]

times = [scipy_time, nevergrad_time]

else:

methods = ['ScipyOptimizer']

final_losses = [scipy_result.fun]

func_evals = [scipy_result.nfev]

times = [scipy_time]

x_pos = np.arange(len(methods))

width = 0.25

# Subplot for metrics

ax2 = axes[1]

ax2_twin = ax2.twinx()

bars1 = ax2.bar(x_pos - width, final_losses, width, label='Final Loss', alpha=0.7, color='blue')

bars2 = ax2.bar(x_pos, func_evals, width, label='Function Evals', alpha=0.7, color='green')

bars3 = ax2_twin.bar(x_pos + width, times, width, label='Time (s)', alpha=0.7, color='red')

ax2.set_xlabel('Method')

ax2.set_ylabel('Loss / Function Evaluations')

ax2_twin.set_ylabel('Time (seconds)')

ax2.set_title('Performance Comparison')

ax2.set_xticks(x_pos)

ax2.set_xticklabels(methods)

ax2.set_yscale('log')

# Combine legends

lines1, labels1 = ax2.get_legend_handles_labels()

lines2, labels2 = ax2_twin.get_legend_handles_labels()

ax2.legend(lines1 + lines2, labels1 + labels2, loc='upper right')

plt.tight_layout()

plt.show()

print("\nComparison Summary:")

print("==================")

print("ScipyOptimizer advantages:")

print("- Faster convergence for smooth functions")

print("- Higher precision solutions")

print("- Fewer function evaluations")

print("- Automatic gradient computation")

print("\nNevergradOptimizer advantages:")

print("- Works with non-differentiable functions")

print("- Better for noisy objectives")

print("- More robust to local minima")

print("- Batched evaluation support")

Comparison Summary:

==================

ScipyOptimizer advantages:

- Faster convergence for smooth functions

- Higher precision solutions

- Fewer function evaluations

- Automatic gradient computation

NevergradOptimizer advantages:

- Works with non-differentiable functions

- Better for noisy objectives

- More robust to local minima

- Batched evaluation support

Best Practices and Tips#

Here are some best practices for using the ScipyOptimizer effectively:

1. Choosing the Right Method#

For bounded problems:

L-BFGS-B: Excellent for smooth, unconstrained or box-constrained problemsTNC: Truncated Newton with bounds, good alternative to L-BFGS-B

For constrained problems:

SLSQP: Sequential Least Squares Programming, handles equality and inequality constraintstrust-constr: Modern trust-region method, very robust for constrained optimization

For unconstrained problems:

BFGS: Standard quasi-Newton methodNewton-CG: Uses Hessian information (computed by JAX)CG: Conjugate gradient method

Derivative-free (when gradients unreliable):

Powell: Direction set methodNelder-Mead: Simplex method

# Best Practice 1: Method selection guidelines

print("Method Selection Guidelines:")

print("==========================\n")

guidelines = {

'L-BFGS-B': {

'description': 'Limited-memory BFGS with bounds',

'best_for': 'Smooth functions with box constraints',

'pros': 'Fast, memory-efficient, handles bounds well',

'cons': 'Only handles box constraints'

},

'SLSQP': {

'description': 'Sequential Least Squares Programming',

'best_for': 'Problems with equality/inequality constraints',

'pros': 'Handles general constraints, robust',

'cons': 'Can be slower than L-BFGS-B for simple problems'

},

'TNC': {

'description': 'Truncated Newton with bounds',

'best_for': 'Alternative to L-BFGS-B for bounded problems',

'pros': 'Good convergence properties, handles bounds',

'cons': 'May be slower than L-BFGS-B'

},

'Powell': {

'description': 'Direction set method (derivative-free)',

'best_for': 'When gradients are unreliable or discontinuous',

'pros': 'No gradient computation, robust',

'cons': 'Slower convergence, more function evaluations'

}

}

for method, info in guidelines.items():

print(f"{method}:")

print(f" Description: {info['description']}")

print(f" Best for: {info['best_for']}")

print(f" Pros: {info['pros']}")

print(f" Cons: {info['cons']}\n")

Method Selection Guidelines:

==========================

L-BFGS-B:

Description: Limited-memory BFGS with bounds

Best for: Smooth functions with box constraints

Pros: Fast, memory-efficient, handles bounds well

Cons: Only handles box constraints

SLSQP:

Description: Sequential Least Squares Programming

Best for: Problems with equality/inequality constraints

Pros: Handles general constraints, robust

Cons: Can be slower than L-BFGS-B for simple problems

TNC:

Description: Truncated Newton with bounds

Best for: Alternative to L-BFGS-B for bounded problems

Pros: Good convergence properties, handles bounds

Cons: May be slower than L-BFGS-B

Powell:

Description: Direction set method (derivative-free)

Best for: When gradients are unreliable or discontinuous

Pros: No gradient computation, robust

Cons: Slower convergence, more function evaluations

# Best Practice 2: Proper scaling and conditioning

print("Best Practice 2: Function scaling and conditioning")

print("===============================================\n")

# Example of badly scaled vs well-scaled problems

def badly_scaled_function(x, y):

"""Function with very different scales in x and y directions."""

return 1e6 * (x - 1.0)**2 + 1e-3 * (y - 2.0)**2

def well_scaled_function(x, y):

"""Same function but with similar scales."""

return (x - 1.0)**2 + (y - 2.0)**2

bounds = [(-5.0, 5.0), (-5.0, 5.0)]

print("Testing badly scaled function...")

bad_optimizer = bts.optim.ScipyOptimizer(

loss_fun=badly_scaled_function, bounds=bounds, method='L-BFGS-B'

)

bad_result = bad_optimizer.minimize(n_iter=1)

print(f" Success: {bad_result.success}")

print(f" Function evaluations: {bad_result.nfev}")

print(f" Final loss: {bad_result.fun:.2e}")

print("\nTesting well scaled function...")

good_optimizer = bts.optim.ScipyOptimizer(

loss_fun=well_scaled_function, bounds=bounds, method='L-BFGS-B'

)

good_result = good_optimizer.minimize(n_iter=1)

print(f" Success: {good_result.success}")

print(f" Function evaluations: {good_result.nfev}")

print(f" Final loss: {good_result.fun:.2e}")

print("\nScaling Tips:")

print("- Normalize parameters to similar ranges (e.g., [-1, 1] or [0, 1])")

print("- Scale the objective function to have reasonable magnitude (≈1)")

print("- Use proper units with BrainUnit to maintain physical meaning")

print("- Consider the condition number of the Hessian matrix")

Best Practice 2: Function scaling and conditioning

===============================================

Testing badly scaled function...

Success: True

Function evaluations: 15

Final loss: 2.00e-04

Testing well scaled function...

Success: True

Function evaluations: 3

Final loss: 3.55e-15

Scaling Tips:

- Normalize parameters to similar ranges (e.g., [-1, 1] or [0, 1])

- Scale the objective function to have reasonable magnitude (≈1)

- Use proper units with BrainUnit to maintain physical meaning

- Consider the condition number of the Hessian matrix

# Best Practice 3: Handling multiple local minima

print("\nBest Practice 3: Multiple starting points for global optimization")

print("=============================================================\n")

def multimodal_function(x, y):

"""Function with multiple local minima."""

return (x**2 + y**2) * (1 + 0.3 * jnp.cos(5*x) * jnp.cos(5*y))

bounds = [(-3.0, 3.0), (-3.0, 3.0)]

# Single optimization run

single_optimizer = bts.optim.ScipyOptimizer(

loss_fun=multimodal_function, bounds=bounds, method='L-BFGS-B'

)

single_result = single_optimizer.minimize(n_iter=1)

# Multiple optimization runs

multi_optimizer = bts.optim.ScipyOptimizer(

loss_fun=multimodal_function, bounds=bounds, method='L-BFGS-B'

)

multi_result = multi_optimizer.minimize(n_iter=10) # Try 10 different starting points

print(f"Single run result:")

print(f" Final loss: {single_result.fun:.6f}")

print(f" Parameters: ({single_result.x[0]:.4f}, {single_result.x[1]:.4f})")

print(f"\nMultiple runs result:")

print(f" Final loss: {multi_result.fun:.6f}")

print(f" Parameters: ({multi_result.x[0]:.4f}, {multi_result.x[1]:.4f})")

print(f"\nImprovement: {(single_result.fun - multi_result.fun) / single_result.fun * 100:.1f}%")

print("\nMultiple Starting Point Tips:")

print("- Always use n_iter > 1 for problems with multiple local minima")

print("- ScipyOptimizer automatically samples different starting points")

print("- For gradient-based methods, combine with derivative-free global search")

print("- Consider using NevergradOptimizer for highly multimodal problems")

Best Practice 3: Multiple starting points for global optimization

=============================================================

Single run result:

Final loss: 0.000000

Parameters: (-0.0000, 0.0000)

Multiple runs result:

Final loss: 0.000000

Parameters: (-0.0000, -0.0000)

Improvement: 99.9%

Multiple Starting Point Tips:

- Always use n_iter > 1 for problems with multiple local minima

- ScipyOptimizer automatically samples different starting points

- For gradient-based methods, combine with derivative-free global search

- Consider using NevergradOptimizer for highly multimodal problems

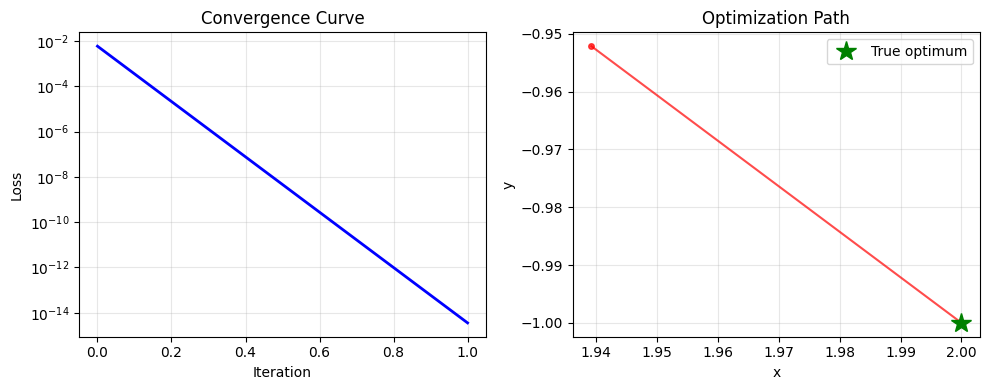

# Best Practice 4: Convergence monitoring and debugging

print("\nBest Practice 4: Monitoring and debugging optimization")

print("===================================================\n")

def monitored_optimization_example():

"""Example showing how to monitor optimization progress."""

# Function to optimize

def objective(x, y):

return (x - 2.0)**2 + (y + 1.0)**2

# Storage for monitoring

iteration_data = []

def callback(x_current):

"""Callback function to monitor progress."""

loss_val = objective(x_current[0], x_current[1])

iteration_data.append({

'x': x_current[0],

'y': x_current[1],

'loss': loss_val

})

# Print every few iterations

if len(iteration_data) % 5 == 0:

print(f" Iteration {len(iteration_data)}: loss = {loss_val:.6f}, x = ({x_current[0]:.4f}, {x_current[1]:.4f})")

# Create optimizer with callback

optimizer = bts.optim.ScipyOptimizer(

loss_fun=objective,

bounds=[(-5.0, 5.0), (-3.0, 3.0)],

method='L-BFGS-B',

callback=callback,

options={'disp': True} # Enable SciPy's own display

)

print("Running monitored optimization...")

result = optimizer.minimize(n_iter=1)

print(f"\nOptimization completed!")

print(f"Total callback calls: {len(iteration_data)}")

print(f"Final result: success = {result.success}, loss = {result.fun:.8f}")

# Plot convergence if we have data

if iteration_data:

losses = [data['loss'] for data in iteration_data]

plt.figure(figsize=(10, 4))

plt.subplot(1, 2, 1)

plt.plot(losses, 'b-', linewidth=2)

plt.xlabel('Iteration')

plt.ylabel('Loss')

plt.title('Convergence Curve')

plt.yscale('log')

plt.grid(True, alpha=0.3)

plt.subplot(1, 2, 2)

x_vals = [data['x'] for data in iteration_data]

y_vals = [data['y'] for data in iteration_data]

plt.plot(x_vals, y_vals, 'ro-', alpha=0.7, markersize=4)

plt.plot(2.0, -1.0, 'g*', markersize=15, label='True optimum')

plt.xlabel('x')

plt.ylabel('y')

plt.title('Optimization Path')

plt.legend()

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

monitored_optimization_example()

print("\nMonitoring Tips:")

print("- Use callback functions to track optimization progress")

print("- Set options={'disp': True} to see SciPy's internal messages")

print("- Check result.success and result.message for convergence info")

print("- Monitor both function values and parameter changes")

print("- Use visualization to understand optimization behavior")

Best Practice 4: Monitoring and debugging optimization

===================================================

Running monitored optimization...

Optimization completed!

Total callback calls: 2

Final result: success = True, loss = 0.00000000

Monitoring Tips:

- Use callback functions to track optimization progress

- Set options={'disp': True} to see SciPy's internal messages

- Check result.success and result.message for convergence info

- Monitor both function values and parameter changes

- Use visualization to understand optimization behavior

Summary#

In this tutorial, we’ve covered the key aspects of using BrainTools’ ScipyOptimizer:

Key Features:

Automatic differentiation: JAX computes gradients automatically

Flexible parameter structures: Support for scalars, arrays, and named parameters

Unit integration: Seamless work with BrainUnit quantities

Multiple algorithms: Access to SciPy’s extensive optimization methods

Constraints: Support for equality and inequality constraints

Advanced options: Custom tolerances, callbacks, and solver-specific options

Best Practices:

Choose the right method - Match the algorithm to your problem characteristics

Scale properly - Normalize parameters and objective function

Use multiple starting points - Set

n_iter > 1for global optimizationMonitor convergence - Use callbacks and check optimization results

When to Use ScipyOptimizer:

Smooth, differentiable objectives where gradients are reliable

High-precision optimization where exact solutions are important

Constrained optimization problems with equality/inequality constraints

Neural network parameter optimization and model fitting

Physics-based models with analytical structure

When to Consider Alternatives:

Noisy objectives → Use NevergradOptimizer

Discontinuous functions → Use derivative-free methods

Very high-dimensional problems → Consider specialized methods

Multiple local minima → Combine with global optimization

The ScipyOptimizer provides a powerful and mature interface for gradient-based optimization in the BrainTools ecosystem, making it ideal for scientific computing and machine learning applications where precision and efficiency are paramount.