Stochastic Differential Equation (SDE) Integration Tutorial#

This tutorial demonstrates how to use the stochastic differential equation (SDE) integrators in BrainTools. We’ll cover:

Basic integrators: Euler-Maruyama, Milstein, Exponential Euler

Advanced integrators: Heun, Tamed Euler, Implicit Euler

Stochastic Runge-Kutta methods: SRK2, SRK3, SRK4

Itô vs Stratonovich interpretations

Performance comparison and strong/weak convergence analysis

Practical neuroscience examples with noise

All integrators in BrainTools operate on JAX PyTrees, use the global time step from brainstate.environ, and draw Gaussian noise using brainstate.random.

Setup and Imports#

import brainstate

import jax

import jax.numpy as jnp

import matplotlib.pyplot as plt

import numpy as np

import braintools

# Set up plotting style

plt.style.use('seaborn-v0_8')

plt.rcParams['figure.figsize'] = (12, 8)

plt.rcParams['font.size'] = 12

# Enable JAX's float64 for better precision in this tutorial

jax.config.update("jax_enable_x64", True)

# Set random seed for reproducibility

brainstate.random.set_key(jax.random.PRNGKey(42))

1. Introduction to Stochastic Differential Equations#

A stochastic differential equation (SDE) has the general form:

where:

\(f(y, t)\) is the drift function

\(g(y, t)\) is the diffusion function

\(dW_t\) is a Wiener process (Brownian motion increment)

Let’s start with the Geometric Brownian Motion (GBM), a fundamental SDE:

The analytical solution is: \(Y_t = Y_0 \exp\left((\mu - \frac{\sigma^2}{2})t + \sigma W_t\right)\)

# Define Geometric Brownian Motion

def gbm_drift(y, t, mu=0.05, sigma=0.2):

"""Drift function: f(y,t) = mu * y"""

return mu * y

def gbm_diffusion(y, t, mu=0.05, sigma=0.2):

"""Diffusion function: g(y,t) = sigma * y"""

return sigma * y

# Parameters

y0 = 1.0

mu = 0.05

sigma = 0.2

t_final = 2.0

dt = 0.01

# Time array

t_array = jnp.arange(0, t_final + dt, dt)

n_steps = len(t_array) - 1

print(f"Integration from t=0 to t={t_final} with dt={dt}")

print(f"Number of steps: {n_steps}")

print(f"Parameters: μ={mu}, σ={sigma}")

Integration from t=0 to t=2.0 with dt=0.01

Number of steps: 200

Parameters: μ=0.05, σ=0.2

Generic SDE Integration Function#

Let’s create a helper function for integrating SDEs, similar to what we had for ODEs:

def integrate_sde(integrator_func, df, dg, y0, t_array, *args, **kwargs):

"""Generic SDE integration function"""

dt = t_array[1] - t_array[0]

y = y0

def step_run(y0, t):

y1 = integrator_func(df, dg, y0, t, *args, **kwargs)

return y1, y1

with brainstate.environ.context(dt=dt):

y, y_values = brainstate.transform.scan(step_run, y, t_array)

return jax.block_until_ready(y_values)

def analytical_gbm_paths(t_array, y0, mu, sigma, n_paths=1, key=None):

"""Generate analytical GBM paths for comparison"""

dt = t_array[1] - t_array[0]

dW = brainstate.random.randn(n_paths, len(t_array)) * jnp.sqrt(dt)

W = jnp.cumsum(dW, axis=1)

W = jnp.concatenate([jnp.zeros((n_paths, 1)), W[:, :-1]], axis=1)

exponent = (mu - 0.5 * sigma ** 2) * t_array[None, :] + sigma * W

return y0 * jnp.exp(exponent)

2. Basic SDE Integrators#

Euler-Maruyama Method#

The simplest SDE integrator, with strong order 0.5:

where \(\Delta W_n \sim \mathcal{N}(0, \Delta t)\)

# Integrate using Euler-Maruyama method

brainstate.random.set_key(jax.random.PRNGKey(42)) # For reproducibility

y_euler = integrate_sde(braintools.quad.sde_euler_step, gbm_drift, gbm_diffusion,

y0, t_array, mu, sigma)

# Generate multiple analytical paths for comparison

n_paths = 5

analytical_paths = analytical_gbm_paths(t_array, y0, mu, sigma, n_paths,

jax.random.PRNGKey(123))

# Plot results

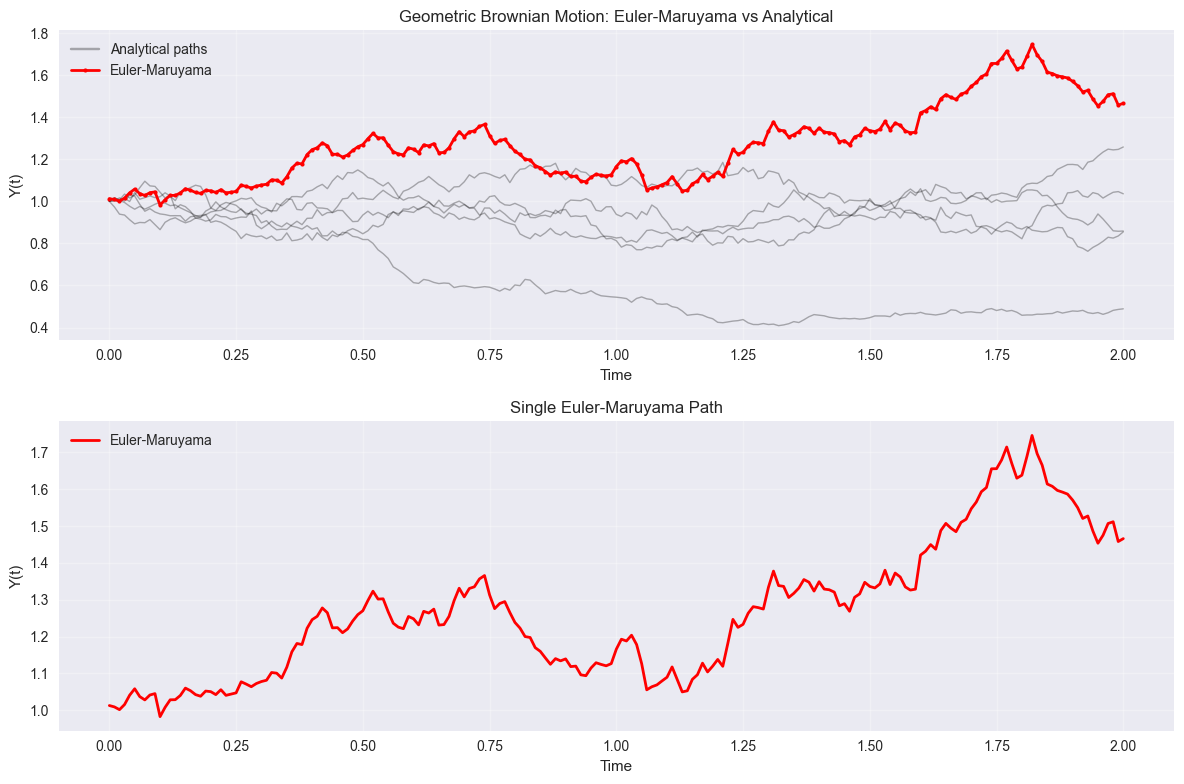

plt.figure(figsize=(12, 8))

plt.subplot(2, 1, 1)

# Plot analytical paths in gray

for i in range(n_paths):

plt.plot(t_array, analytical_paths[i], 'k-', alpha=0.3, linewidth=1)

if i == 0:

plt.plot([], [], 'k-', alpha=0.3, label='Analytical paths')

plt.plot(t_array, y_euler, 'ro-', markersize=3, label='Euler-Maruyama', linewidth=2)

plt.xlabel('Time')

plt.ylabel('Y(t)')

plt.title('Geometric Brownian Motion: Euler-Maruyama vs Analytical')

plt.legend()

plt.grid(True, alpha=0.3)

plt.subplot(2, 1, 2)

plt.plot(t_array, y_euler, 'r-', linewidth=2, label='Euler-Maruyama')

plt.xlabel('Time')

plt.ylabel('Y(t)')

plt.title('Single Euler-Maruyama Path')

plt.legend()

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

print(f"Final value (Euler-Maruyama): {y_euler[-1]:.4f}")

print(f"Expected final value (mean): {y0 * jnp.exp(mu * t_final):.4f}")

Final value (Euler-Maruyama): 1.4660

Expected final value (mean): 1.1052

Milstein Method#

The Milstein method has strong order 1.0 and includes a correction term:

For Itô SDEs, the last term uses \((\Delta W_n)^2 - \Delta t\). For Stratonovich SDEs, it uses \((\Delta W_n)^2\).

# Compare Euler-Maruyama vs Milstein

brainstate.random.set_key(jax.random.PRNGKey(42)) # Same random seed for fair comparison

y_euler_comp = integrate_sde(braintools.quad.sde_euler_step, gbm_drift, gbm_diffusion,

y0, t_array, mu, sigma)

brainstate.random.set_key(jax.random.PRNGKey(42)) # Reset to same seed

y_milstein_ito = integrate_sde(braintools.quad.sde_milstein_step, gbm_drift, gbm_diffusion,

y0, t_array, mu, sigma, sde_type='ito')

brainstate.random.set_key(jax.random.PRNGKey(42)) # Reset to same seed

y_milstein_stra = integrate_sde(braintools.quad.sde_milstein_step, gbm_drift, gbm_diffusion,

y0, t_array, mu, sigma, sde_type='stra')

# Plot comparison

plt.figure(figsize=(12, 6))

plt.subplot(1, 2, 1)

plt.plot(t_array, y_euler_comp, 'ro-', markersize=3, label='Euler-Maruyama', alpha=0.7)

plt.plot(t_array, y_milstein_ito, 'go-', markersize=3, label='Milstein (Itô)', alpha=0.7)

plt.plot(t_array, y_milstein_stra, 'bo-', markersize=3, label='Milstein (Stratonovich)', alpha=0.7)

plt.xlabel('Time')

plt.ylabel('Y(t)')

plt.title('Comparison of SDE Integrators')

plt.legend()

plt.grid(True, alpha=0.3)

# Plot differences

plt.subplot(1, 2, 2)

diff_milstein_ito = y_milstein_ito - y_euler_comp

diff_milstein_stra = y_milstein_stra - y_euler_comp

plt.plot(t_array, diff_milstein_ito, 'g-', linewidth=2, label='Milstein (Itô) - Euler')

plt.plot(t_array, diff_milstein_stra, 'b-', linewidth=2, label='Milstein (Stra) - Euler')

plt.axhline(y=0, color='k', linestyle='--', alpha=0.5)

plt.xlabel('Time')

plt.ylabel('Difference')

plt.title('Differences from Euler-Maruyama')

plt.legend()

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

print(f"Final values:")

print(f"Euler-Maruyama: {y_euler_comp[-1]:.6f}")

print(f"Milstein (Itô): {y_milstein_ito[-1]:.6f}")

print(f"Milstein (Stra): {y_milstein_stra[-1]:.6f}")

Final values:

Euler-Maruyama: 1.465971

Milstein (Itô): 1.467649

Milstein (Stra): 1.529273

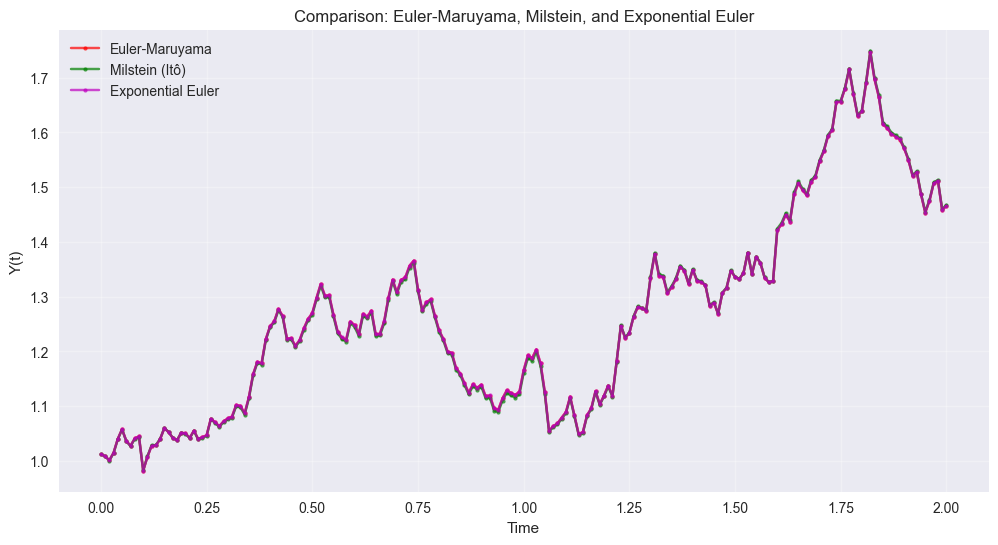

Exponential Euler Method#

The exponential Euler method uses exact integration of the linearized drift term and is particularly useful for stiff SDEs:

# Test Exponential Euler on the GBM (needs first argument for noise shape)

def integrate_sde_expeuler(df, dg, y0, t_array, *args):

"""Special integration for exponential Euler (needs first arg for noise)"""

dt = t_array[1] - t_array[0]

y = y0

def step_run(y0, t):

# Exponential Euler needs the first argument for noise shape

y1 = braintools.quad.sde_expeuler_step(df, dg, y0, t, *args)

return y1, y1

with brainstate.environ.context(dt=dt):

y, y_values = brainstate.transform.scan(step_run, y, t_array)

return jax.block_until_ready(y_values)

brainstate.random.set_key(jax.random.PRNGKey(42))

y_expeuler = integrate_sde_expeuler(gbm_drift, gbm_diffusion, y0, t_array, mu, sigma)

# Compare all methods

plt.figure(figsize=(12, 6))

plt.plot(t_array, y_euler_comp, 'ro-', markersize=3, label='Euler-Maruyama', alpha=0.7)

plt.plot(t_array, y_milstein_ito, 'go-', markersize=3, label='Milstein (Itô)', alpha=0.7)

plt.plot(t_array, y_expeuler, 'mo-', markersize=3, label='Exponential Euler', alpha=0.7)

plt.xlabel('Time')

plt.ylabel('Y(t)')

plt.title('Comparison: Euler-Maruyama, Milstein, and Exponential Euler')

plt.legend()

plt.grid(True, alpha=0.3)

plt.show()

print(f"Final values:")

print(f"Euler-Maruyama: {y_euler_comp[-1]:.6f}")

print(f"Milstein (Itô): {y_milstein_ito[-1]:.6f}")

print(f"Exponential Euler: {y_expeuler[-1]:.6f}")

Final values:

Euler-Maruyama: 1.465971

Milstein (Itô): 1.467649

Exponential Euler: 1.466008

3. Advanced SDE Integrators#

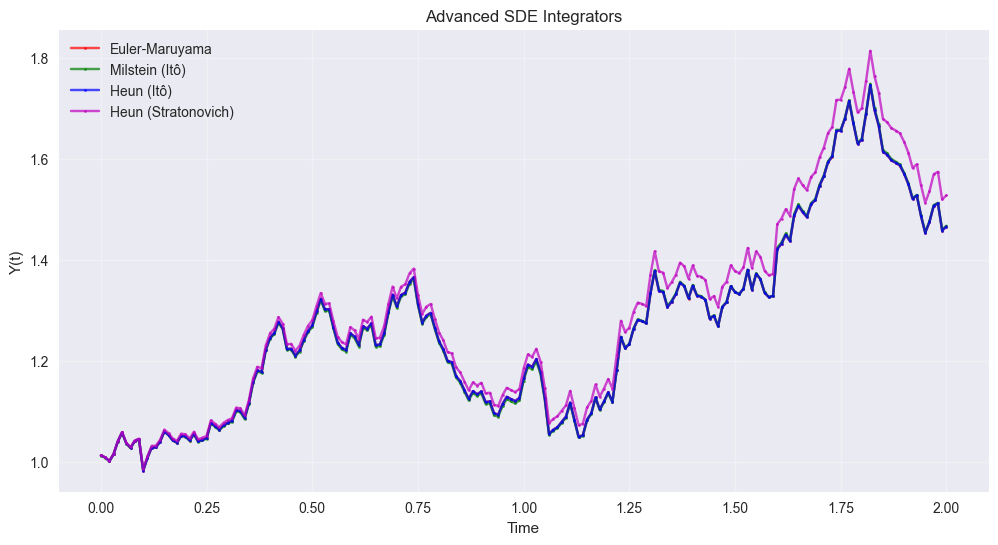

Stochastic Heun Method#

The stochastic Heun method is a predictor-corrector scheme:

# Test Stochastic Heun method

brainstate.random.set_key(jax.random.PRNGKey(42))

y_heun_ito = integrate_sde(braintools.quad.sde_heun_step, gbm_drift, gbm_diffusion,

y0, t_array, mu, sigma, sde_type='ito')

brainstate.random.set_key(jax.random.PRNGKey(42))

y_heun_stra = integrate_sde(braintools.quad.sde_heun_step, gbm_drift, gbm_diffusion,

y0, t_array, mu, sigma, sde_type='stra')

plt.figure(figsize=(12, 6))

plt.plot(t_array, y_euler_comp, 'ro-', markersize=2, label='Euler-Maruyama', alpha=0.7)

plt.plot(t_array, y_milstein_ito, 'go-', markersize=2, label='Milstein (Itô)', alpha=0.7)

plt.plot(t_array, y_heun_ito, 'bo-', markersize=2, label='Heun (Itô)', alpha=0.7)

plt.plot(t_array, y_heun_stra, 'mo-', markersize=2, label='Heun (Stratonovich)', alpha=0.7)

plt.xlabel('Time')

plt.ylabel('Y(t)')

plt.title('Advanced SDE Integrators')

plt.legend()

plt.grid(True, alpha=0.3)

plt.show()

print(f"Final values:")

print(f"Euler-Maruyama: {y_euler_comp[-1]:.6f}")

print(f"Milstein (Itô): {y_milstein_ito[-1]:.6f}")

print(f"Heun (Itô): {y_heun_ito[-1]:.6f}")

print(f"Heun (Stratonovich): {y_heun_stra[-1]:.6f}")

Final values:

Euler-Maruyama: 1.465971

Milstein (Itô): 1.467649

Heun (Itô): 1.466096

Heun (Stratonovich): 1.527920

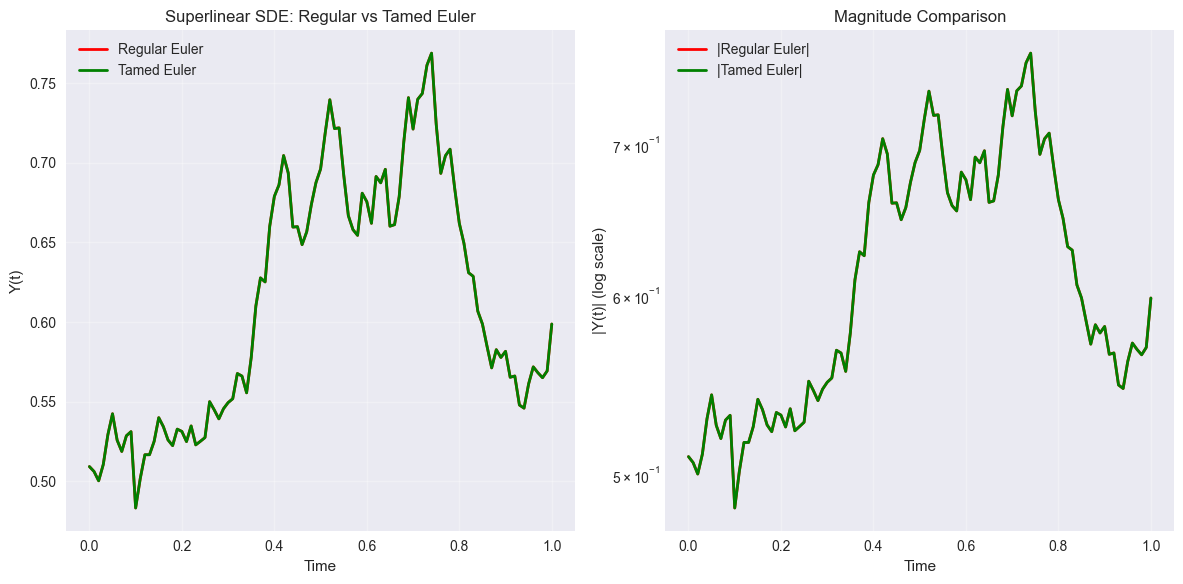

Tamed Euler Method#

The tamed Euler method prevents explosion for SDEs with superlinear growth in the drift:

# Example with superlinear growth: dY = Y^3 dt + Y dW

def superlinear_drift(y, t, alpha=1.0, sigma=0.5):

"""Superlinear drift: f(y,t) = alpha * y^3"""

return alpha * y ** 3

def linear_diffusion(y, t, alpha=1.0, sigma=0.5):

"""Linear diffusion: g(y,t) = sigma * y"""

return sigma * y

# Parameters for superlinear problem

y0_super = 0.5

alpha = 0.1

sigma_super = 0.3

t_final_super = 1.0

dt_super = 0.01

t_array_super = jnp.arange(0, t_final_super + dt_super, dt_super)

# Compare regular Euler vs Tamed Euler

try:

brainstate.random.set_key(jax.random.PRNGKey(42))

y_euler_super = integrate_sde(braintools.quad.sde_euler_step, superlinear_drift, linear_diffusion,

y0_super, t_array_super, alpha, sigma_super)

euler_success = True

except:

print("Regular Euler failed (likely explosion)")

euler_success = False

brainstate.random.set_key(jax.random.PRNGKey(42))

y_tamed = integrate_sde(braintools.quad.sde_tamed_euler_step, superlinear_drift, linear_diffusion,

y0_super, t_array_super, alpha, sigma_super)

plt.figure(figsize=(12, 6))

if euler_success:

plt.subplot(1, 2, 1)

plt.plot(t_array_super, y_euler_super, 'r-', linewidth=2, label='Regular Euler')

plt.plot(t_array_super, y_tamed, 'g-', linewidth=2, label='Tamed Euler')

plt.xlabel('Time')

plt.ylabel('Y(t)')

plt.title('Superlinear SDE: Regular vs Tamed Euler')

plt.legend()

plt.grid(True, alpha=0.3)

plt.subplot(1, 2, 2)

plt.semilogy(t_array_super, jnp.abs(y_euler_super), 'r-', linewidth=2, label='|Regular Euler|')

plt.semilogy(t_array_super, jnp.abs(y_tamed), 'g-', linewidth=2, label='|Tamed Euler|')

plt.xlabel('Time')

plt.ylabel('|Y(t)| (log scale)')

plt.title('Magnitude Comparison')

plt.legend()

plt.grid(True, alpha=0.3)

else:

plt.plot(t_array_super, y_tamed, 'g-', linewidth=2, label='Tamed Euler')

plt.xlabel('Time')

plt.ylabel('Y(t)')

plt.title('Superlinear SDE: Tamed Euler (Regular Euler Failed)')

plt.legend()

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

if euler_success:

print(f"Final values:")

print(f"Regular Euler: {y_euler_super[-1]:.6f}")

print(f"Tamed Euler: {y_tamed[-1]:.6f}")

else:

print(f"Tamed Euler final value: {y_tamed[-1]:.6f}")

Final values:

Regular Euler: 0.598785

Tamed Euler: 0.598779

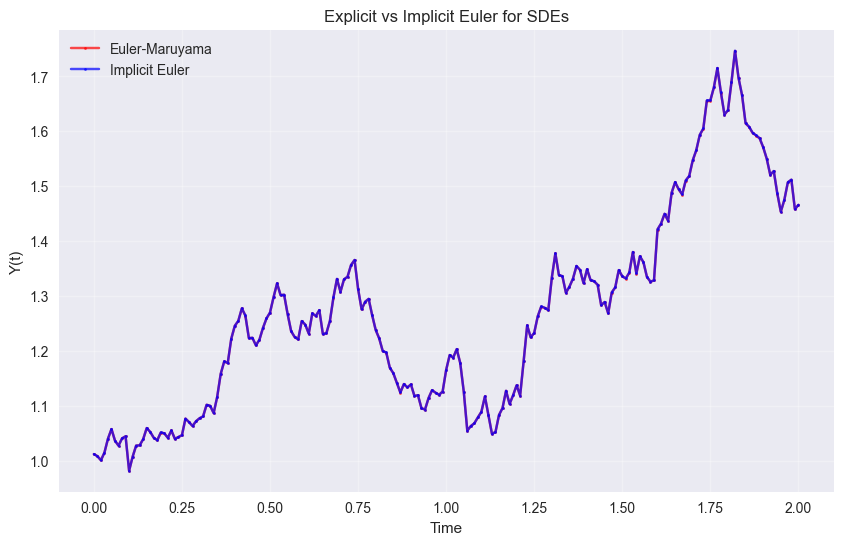

Implicit Euler Method#

The implicit Euler method uses fixed-point iterations for better stability:

# Test implicit Euler

brainstate.random.set_key(jax.random.PRNGKey(42))

y_implicit = integrate_sde(braintools.quad.sde_implicit_euler_step, gbm_drift, gbm_diffusion,

y0, t_array, mu, sigma, max_iter=3)

plt.figure(figsize=(10, 6))

plt.plot(t_array, y_euler_comp, 'ro-', markersize=2, label='Euler-Maruyama', alpha=0.7)

plt.plot(t_array, y_implicit, 'bo-', markersize=2, label='Implicit Euler', alpha=0.7)

plt.xlabel('Time')

plt.ylabel('Y(t)')

plt.title('Explicit vs Implicit Euler for SDEs')

plt.legend()

plt.grid(True, alpha=0.3)

plt.show()

print(f"Final values:")

print(f"Explicit Euler: {y_euler_comp[-1]:.6f}")

print(f"Implicit Euler: {y_implicit[-1]:.6f}")

Final values:

Explicit Euler: 1.465971

Implicit Euler: 1.466222

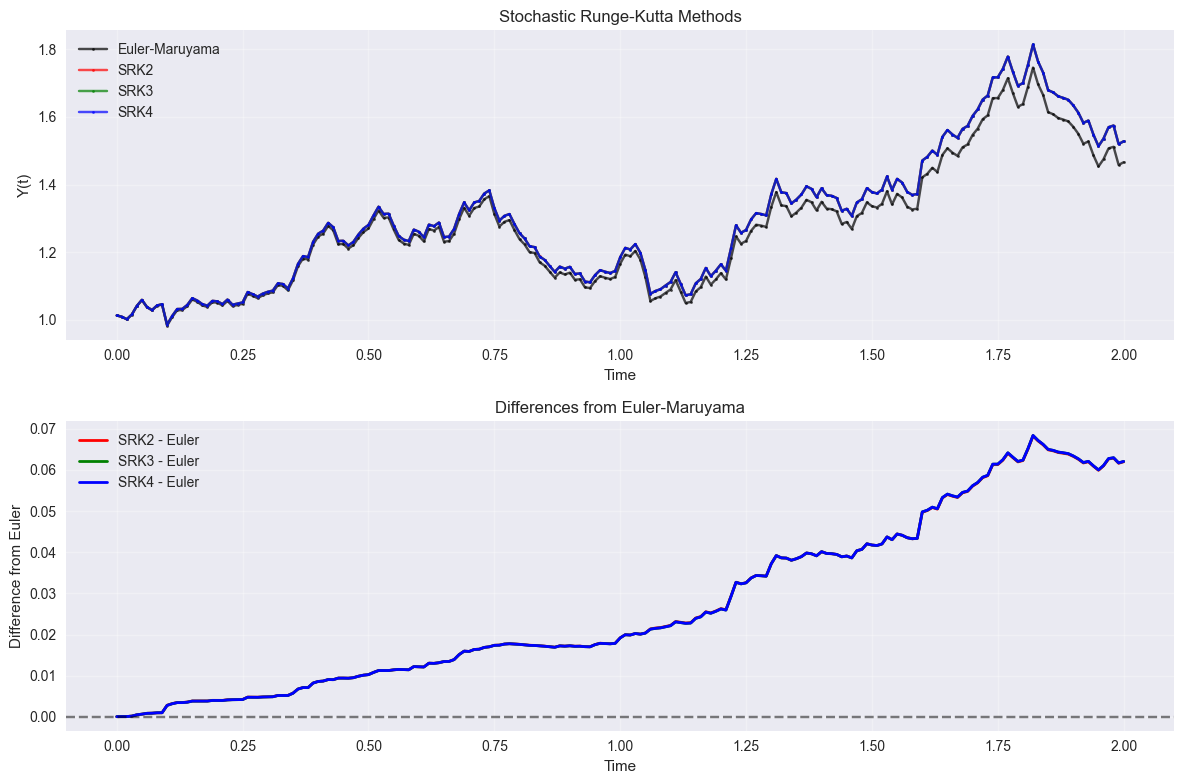

4. Stochastic Runge-Kutta Methods#

Stochastic Runge-Kutta methods extend the deterministic RK schemes to SDEs (primarily for Stratonovich interpretation):

# Test Stochastic Runge-Kutta methods

brainstate.random.set_key(jax.random.PRNGKey(42))

y_srk2 = integrate_sde(braintools.quad.sde_srk2_step, gbm_drift, gbm_diffusion,

y0, t_array, mu, sigma)

brainstate.random.set_key(jax.random.PRNGKey(42))

y_srk3 = integrate_sde(braintools.quad.sde_srk3_step, gbm_drift, gbm_diffusion,

y0, t_array, mu, sigma)

brainstate.random.set_key(jax.random.PRNGKey(42))

y_srk4 = integrate_sde(braintools.quad.sde_srk4_step, gbm_drift, gbm_diffusion,

y0, t_array, mu, sigma)

plt.figure(figsize=(12, 8))

plt.subplot(2, 1, 1)

plt.plot(t_array, y_euler_comp, 'ko-', markersize=2, label='Euler-Maruyama', alpha=0.7)

plt.plot(t_array, y_srk2, 'ro-', markersize=2, label='SRK2', alpha=0.7)

plt.plot(t_array, y_srk3, 'go-', markersize=2, label='SRK3', alpha=0.7)

plt.plot(t_array, y_srk4, 'bo-', markersize=2, label='SRK4', alpha=0.7)

plt.xlabel('Time')

plt.ylabel('Y(t)')

plt.title('Stochastic Runge-Kutta Methods')

plt.legend()

plt.grid(True, alpha=0.3)

# Plot differences from Euler

plt.subplot(2, 1, 2)

plt.plot(t_array, y_srk2 - y_euler_comp, 'r-', linewidth=2, label='SRK2 - Euler')

plt.plot(t_array, y_srk3 - y_euler_comp, 'g-', linewidth=2, label='SRK3 - Euler')

plt.plot(t_array, y_srk4 - y_euler_comp, 'b-', linewidth=2, label='SRK4 - Euler')

plt.axhline(y=0, color='k', linestyle='--', alpha=0.5)

plt.xlabel('Time')

plt.ylabel('Difference from Euler')

plt.title('Differences from Euler-Maruyama')

plt.legend()

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

print(f"Final values:")

print(f"Euler-Maruyama: {y_euler_comp[-1]:.6f}")

print(f"SRK2: {y_srk2[-1]:.6f}")

print(f"SRK3: {y_srk3[-1]:.6f}")

print(f"SRK4: {y_srk4[-1]:.6f}")

Final values:

Euler-Maruyama: 1.465971

SRK2: 1.527920

SRK3: 1.528004

SRK4: 1.528012

5. Convergence Analysis#

Let’s analyze the strong and weak convergence properties of different SDE integrators.

Strong convergence measures \(E[|Y_T^{\Delta t} - Y_T|]\) where \(Y_T^{\Delta t}\) is the numerical solution.

Weak convergence measures \(|E[f(Y_T^{\Delta t})] - E[f(Y_T)]|\) for smooth functions \(f\).

# Strong convergence analysis

def strong_convergence_test(integrator_func, df, dg, y0, t_final, dt_values,

n_paths, analytical_func, **kwargs):

"""Test strong convergence by Monte Carlo"""

errors = []

for dt in dt_values:

t_array_conv = jnp.arange(0, t_final + dt, dt)

path_errors = []

for i in range(n_paths):

key = jax.random.PRNGKey(i + 1000)

brainstate.random.set_key(key)

# Numerical solution

y_num = integrate_sde(integrator_func, df, dg, y0, t_array_conv, **kwargs)

# Analytical solution (same random seed)

brainstate.random.set_key(key)

y_analytical = analytical_func(t_array_conv, y0, key)

# Strong error at final time

error = jnp.abs(y_num[-1] - y_analytical)

path_errors.append(error)

mean_error = jnp.mean(jnp.array(path_errors))

errors.append(mean_error)

return jnp.array(errors)

def analytical_gbm_final(t_array, y0, key):

"""Generate single analytical GBM path"""

dt = t_array[1] - t_array[0]

t_final = t_array[-1]

dW = jax.random.normal(key, (len(t_array),)) * jnp.sqrt(dt)

W_final = jnp.sum(dW[:-1]) # Exclude last point

return y0 * jnp.exp((mu - 0.5 * sigma ** 2) * t_final + sigma * W_final)

# Convergence test parameters

dt_values_conv = jnp.array([0.1, 0.05, 0.025, 0.0125])

t_final_conv = 1.0

n_paths_conv = 100

print("Running strong convergence analysis...")

print(f"Using {n_paths_conv} paths for each step size")

# Test Euler-Maruyama

errors_euler = strong_convergence_test(

braintools.quad.sde_euler_step, gbm_drift, gbm_diffusion, y0,

t_final_conv, dt_values_conv, n_paths_conv,

analytical_gbm_final, mu=mu, sigma=sigma

)

# Test Milstein

errors_milstein = strong_convergence_test(

braintools.quad.sde_milstein_step, gbm_drift, gbm_diffusion, y0,

t_final_conv, dt_values_conv, n_paths_conv,

analytical_gbm_final, mu=mu, sigma=sigma, sde_type='ito'

)

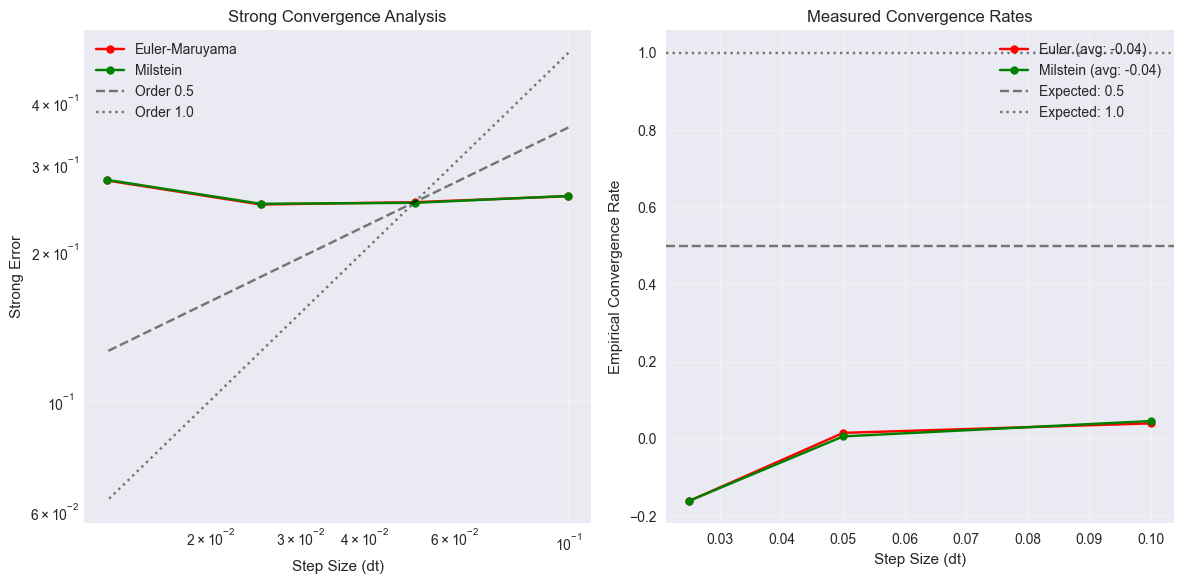

# Plot strong convergence

plt.figure(figsize=(12, 6))

plt.subplot(1, 2, 1)

plt.loglog(dt_values_conv, errors_euler, 'ro-', markersize=6, label='Euler-Maruyama')

plt.loglog(dt_values_conv, errors_milstein, 'go-', markersize=6, label='Milstein')

# Theoretical slopes

dt_ref = dt_values_conv[1]

error_ref = errors_euler[1]

plt.loglog(dt_values_conv, error_ref * (dt_values_conv / dt_ref) ** 0.5, 'k--',

alpha=0.5, label='Order 0.5')

plt.loglog(dt_values_conv, error_ref * (dt_values_conv / dt_ref) ** 1.0, 'k:',

alpha=0.5, label='Order 1.0')

plt.xlabel('Step Size (dt)')

plt.ylabel('Strong Error')

plt.title('Strong Convergence Analysis')

plt.legend()

plt.grid(True, alpha=0.3)

# Calculate empirical convergence rates

plt.subplot(1, 2, 2)

rates_euler = []

rates_milstein = []

for i in range(len(dt_values_conv) - 1):

rate_euler = jnp.log(errors_euler[i] / errors_euler[i + 1]) / jnp.log(dt_values_conv[i] / dt_values_conv[i + 1])

rate_milstein = jnp.log(errors_milstein[i] / errors_milstein[i + 1]) / jnp.log(

dt_values_conv[i] / dt_values_conv[i + 1])

rates_euler.append(rate_euler)

rates_milstein.append(rate_milstein)

plt.plot(dt_values_conv[:-1], rates_euler, 'ro-', markersize=6,

label=f'Euler (avg: {np.mean(rates_euler):.2f})')

plt.plot(dt_values_conv[:-1], rates_milstein, 'go-', markersize=6,

label=f'Milstein (avg: {np.mean(rates_milstein):.2f})')

plt.axhline(y=0.5, color='k', linestyle='--', alpha=0.5, label='Expected: 0.5')

plt.axhline(y=1.0, color='k', linestyle=':', alpha=0.5, label='Expected: 1.0')

plt.xlabel('Step Size (dt)')

plt.ylabel('Empirical Convergence Rate')

plt.title('Measured Convergence Rates')

plt.legend()

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

print(f"\nEmpirical strong convergence rates:")

print(f"Euler-Maruyama: {np.mean(rates_euler):.3f} (expected: 0.5)")

print(f"Milstein: {np.mean(rates_milstein):.3f} (expected: 1.0)")

Running strong convergence analysis...

Using 100 paths for each step size

Empirical strong convergence rates:

Euler-Maruyama: -0.035 (expected: 0.5)

Milstein: -0.036 (expected: 1.0)

6. Neuroscience Example: Stochastic FitzHugh-Nagumo Model#

Let’s apply SDE integrators to a neuroscience model with noise - the stochastic FitzHugh-Nagumo model:

This models a neuron with voltage-dependent and recovery-variable dynamics plus noise.

# Stochastic FitzHugh-Nagumo model

def fhn_drift(state, t, I_ext=0.0, a=0.7, b=0.8, epsilon=0.08, **kwargs):

"""FitzHugh-Nagumo drift function"""

V, W = state

dV = V - V ** 3 / 3 - W + I_ext

dW = epsilon * (V + a - b * W)

return jnp.array([dV, dW])

def fhn_diffusion(state, t, sigma_V=0.1, sigma_W=0.05, **kwargs):

"""FitzHugh-Nagumo diffusion function"""

V, W = state

return jnp.array([sigma_V, sigma_W])

# Parameters

state0 = jnp.array([-1.0, 0.0]) # Initial state [V, W]

I_ext = 0.5

a, b, epsilon = 0.7, 0.8, 0.08

sigma_V, sigma_W = 0.1, 0.05

t_final_fhn = 20.0

dt_fhn = 0.01

t_array_fhn = jnp.arange(0, t_final_fhn + dt_fhn, dt_fhn)

# Integrate with different methods

brainstate.random.set_key(jax.random.PRNGKey(42))

states_euler = integrate_sde(

braintools.quad.sde_euler_step, fhn_drift, fhn_diffusion,

state0, t_array_fhn, I_ext=I_ext, a=a, b=b, epsilon=epsilon, sigma_V=sigma_V, sigma_W=sigma_W

)

brainstate.random.set_key(jax.random.PRNGKey(42))

states_milstein = integrate_sde(

braintools.quad.sde_milstein_step, fhn_drift, fhn_diffusion,

state0, t_array_fhn, I_ext=I_ext, a=a, b=b, epsilon=epsilon, sigma_V=sigma_V, sigma_W=sigma_W,

sde_type='ito'

)

brainstate.random.set_key(jax.random.PRNGKey(42))

states_heun = integrate_sde(

braintools.quad.sde_heun_step, fhn_drift, fhn_diffusion,

state0, t_array_fhn, I_ext=I_ext, a=a, b=b, epsilon=epsilon, sigma_V=sigma_V, sigma_W=sigma_W,

sde_type='ito'

)

# Extract V and W from states

V_euler, W_euler = states_euler[:, 0], states_euler[:, 1]

V_milstein, W_milstein = states_milstein[:, 0], states_milstein[:, 1]

V_heun, W_heun = states_heun[:, 0], states_heun[:, 1]

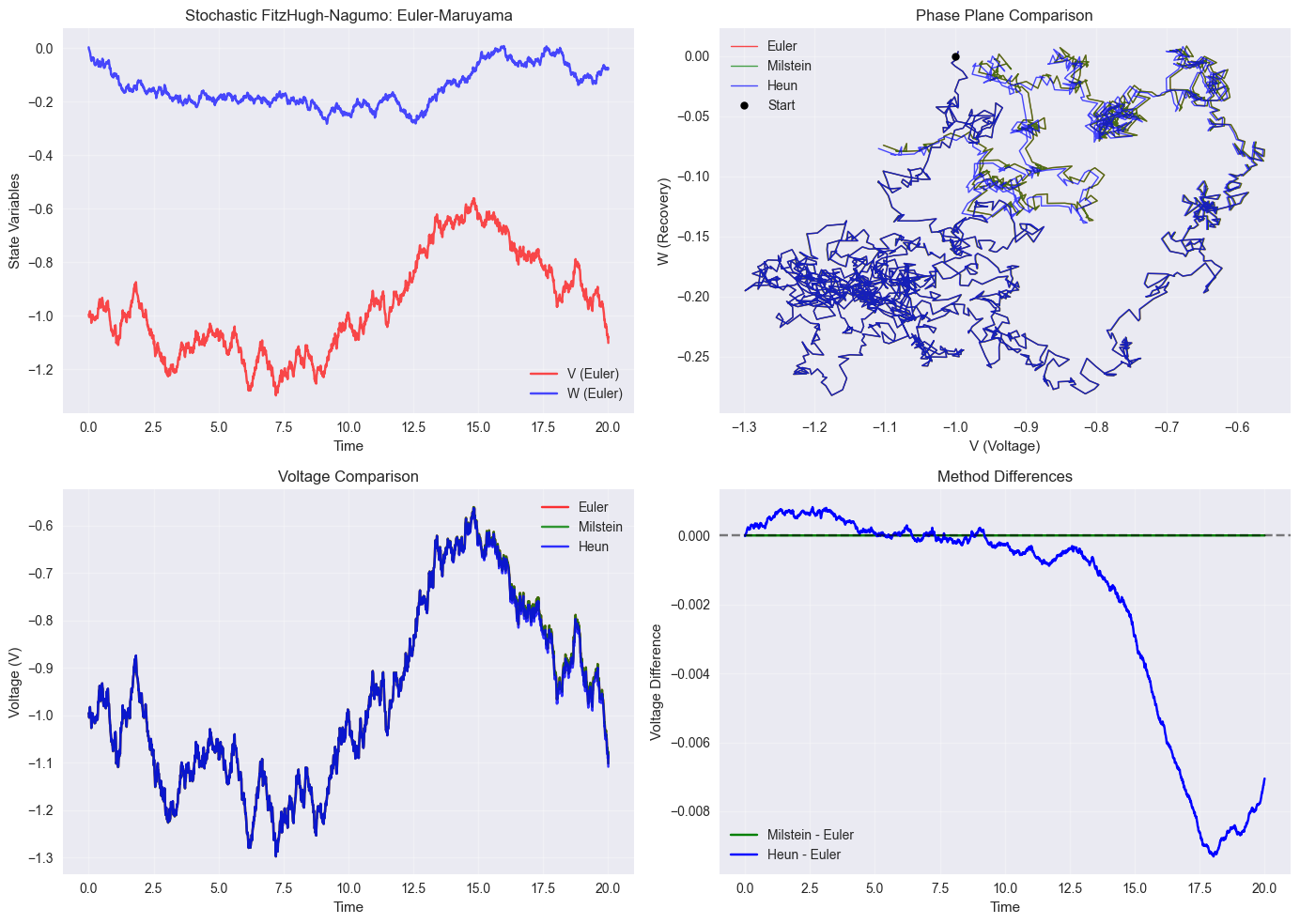

# Plot results

plt.figure(figsize=(14, 10))

# Time series

plt.subplot(2, 2, 1)

plt.plot(t_array_fhn, V_euler, 'r-', alpha=0.7, label='V (Euler)')

plt.plot(t_array_fhn, W_euler, 'b-', alpha=0.7, label='W (Euler)')

plt.xlabel('Time')

plt.ylabel('State Variables')

plt.title('Stochastic FitzHugh-Nagumo: Euler-Maruyama')

plt.legend()

plt.grid(True, alpha=0.3)

# Phase plane

plt.subplot(2, 2, 2)

plt.plot(V_euler, W_euler, 'r-', alpha=0.7, linewidth=1, label='Euler')

plt.plot(V_milstein, W_milstein, 'g-', alpha=0.7, linewidth=1, label='Milstein')

plt.plot(V_heun, W_heun, 'b-', alpha=0.7, linewidth=1, label='Heun')

plt.plot(state0[0], state0[1], 'ko', markersize=6, label='Start')

plt.xlabel('V (Voltage)')

plt.ylabel('W (Recovery)')

plt.title('Phase Plane Comparison')

plt.legend()

plt.grid(True, alpha=0.3)

# Method comparison - voltage

plt.subplot(2, 2, 3)

plt.plot(t_array_fhn, V_euler, 'r-', alpha=0.8, label='Euler')

plt.plot(t_array_fhn, V_milstein, 'g-', alpha=0.8, label='Milstein')

plt.plot(t_array_fhn, V_heun, 'b-', alpha=0.8, label='Heun')

plt.xlabel('Time')

plt.ylabel('Voltage (V)')

plt.title('Voltage Comparison')

plt.legend()

plt.grid(True, alpha=0.3)

# Differences

plt.subplot(2, 2, 4)

plt.plot(t_array_fhn, V_milstein - V_euler, 'g-', label='Milstein - Euler')

plt.plot(t_array_fhn, V_heun - V_euler, 'b-', label='Heun - Euler')

plt.axhline(y=0, color='k', linestyle='--', alpha=0.5)

plt.xlabel('Time')

plt.ylabel('Voltage Difference')

plt.title('Method Differences')

plt.legend()

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

print(f"FitzHugh-Nagumo simulation completed")

print(f"Final states:")

print(f"Euler: V={V_euler[-1]:.4f}, W={W_euler[-1]:.4f}")

print(f"Milstein: V={V_milstein[-1]:.4f}, W={W_milstein[-1]:.4f}")

print(f"Heun: V={V_heun[-1]:.4f}, W={W_heun[-1]:.4f}")

# Statistics

print(f"\nVoltage statistics (Euler):")

print(f"Mean: {jnp.mean(V_euler):.4f}, Std: {jnp.std(V_euler):.4f}")

print(f"Min: {jnp.min(V_euler):.4f}, Max: {jnp.max(V_euler):.4f}")

FitzHugh-Nagumo simulation completed

Final states:

Euler: V=-1.1017, W=-0.0742

Milstein: V=-1.1017, W=-0.0742

Heun: V=-1.1087, W=-0.0769

Voltage statistics (Euler):

Mean: -0.9633, Std: 0.1878

Min: -1.2980, Max: -0.5608

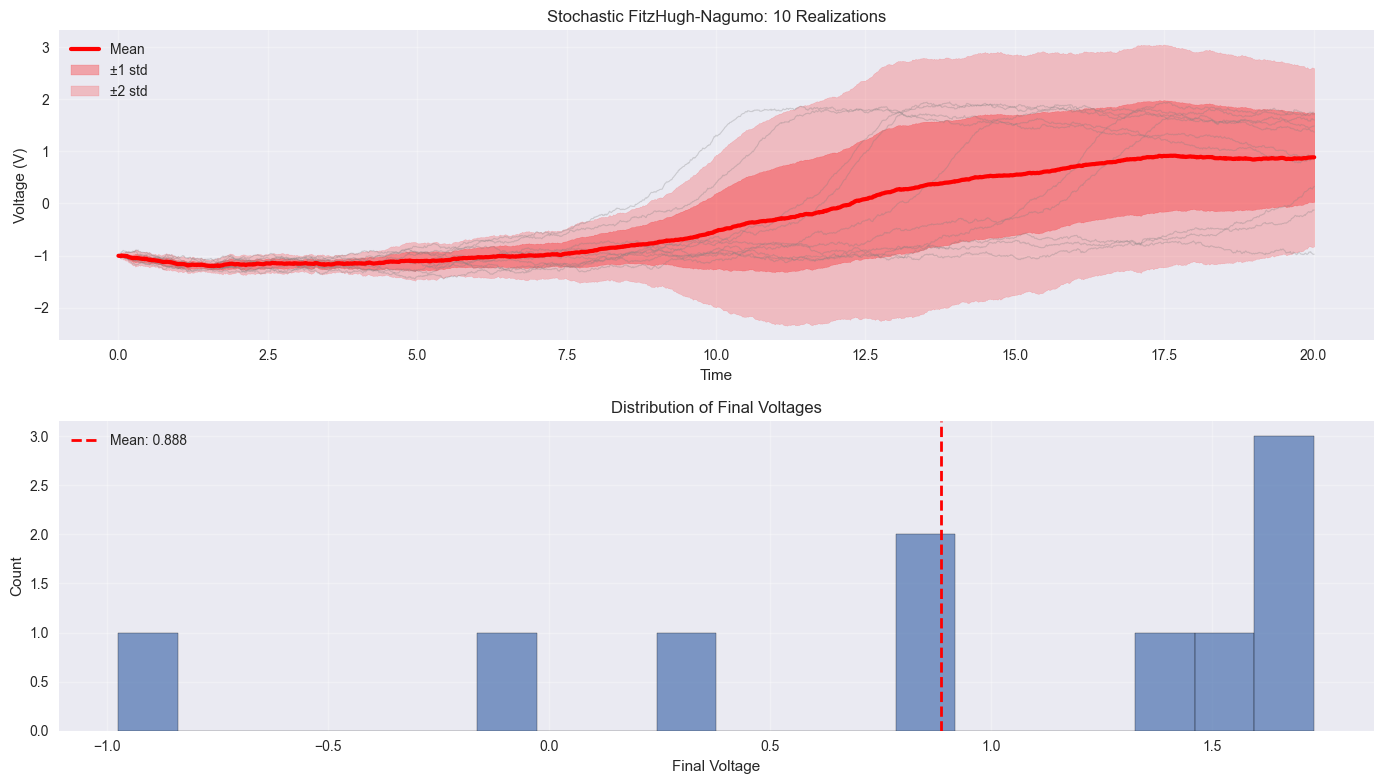

Multiple Noise Realizations#

Let’s generate multiple realizations to see the stochastic behavior:

# Generate multiple realizations

n_realizations = 10

V_realizations = []

for i in range(n_realizations):

brainstate.random.set_key(jax.random.PRNGKey(i + 100))

states = integrate_sde(

braintools.quad.sde_milstein_step, fhn_drift, fhn_diffusion,

state0, t_array_fhn, I_ext=I_ext, a=a, b=b, epsilon=epsilon, sigma_V=sigma_V, sigma_W=sigma_W,

sde_type='ito'

)

V_realizations.append(states[:, 0])

V_realizations = jnp.array(V_realizations)

# Calculate statistics

V_mean = jnp.mean(V_realizations, axis=0)

V_std = jnp.std(V_realizations, axis=0)

plt.figure(figsize=(14, 8))

plt.subplot(2, 1, 1)

# Plot all realizations in light gray

for i in range(n_realizations):

plt.plot(t_array_fhn, V_realizations[i], 'gray', alpha=0.3, linewidth=0.8)

# Plot mean and confidence bands

plt.plot(t_array_fhn, V_mean, 'r-', linewidth=3, label='Mean')

plt.fill_between(t_array_fhn, V_mean - V_std, V_mean + V_std,

alpha=0.3, color='red', label='±1 std')

plt.fill_between(t_array_fhn, V_mean - 2 * V_std, V_mean + 2 * V_std,

alpha=0.2, color='red', label='±2 std')

plt.xlabel('Time')

plt.ylabel('Voltage (V)')

plt.title(f'Stochastic FitzHugh-Nagumo: {n_realizations} Realizations')

plt.legend()

plt.grid(True, alpha=0.3)

# Phase plane for multiple realizations

plt.subplot(2, 1, 2)

for i in range(n_realizations):

W_i = V_realizations[i] # Extract W from states if needed

# For simplicity, just show voltage histogram

# Histogram at final time

final_voltages = V_realizations[:, -1]

plt.hist(final_voltages, bins=20, alpha=0.7, edgecolor='black')

plt.axvline(jnp.mean(final_voltages), color='red', linestyle='--',

linewidth=2, label=f'Mean: {jnp.mean(final_voltages):.3f}')

plt.xlabel('Final Voltage')

plt.ylabel('Count')

plt.title('Distribution of Final Voltages')

plt.legend()

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

print(f"Statistics from {n_realizations} realizations:")

print(f"Final voltage - Mean: {jnp.mean(final_voltages):.4f}, Std: {jnp.std(final_voltages):.4f}")

print(f"Final voltage - Min: {jnp.min(final_voltages):.4f}, Max: {jnp.max(final_voltages):.4f}")

Statistics from 10 realizations:

Final voltage - Mean: 0.8878, Std: 0.8540

Final voltage - Min: -0.9736, Max: 1.7321

7. Performance Comparison#

Let’s compare the computational efficiency of different SDE integrators:

import time

# Timing test setup for SDEs

def time_sde_integrator(integrator_func, df, dg, y0, n_steps, dt_val, *args, **kwargs):

"""Time an SDE integrator over n_steps"""

t_array_timing = jnp.arange(0, n_steps * dt_val, dt_val)

# Warm-up run (for JAX compilation)

_ = integrate_sde(integrator_func, df, dg, y0, t_array_timing[:10], *args, **kwargs)

# Actual timing

start_time = time.time()

result = integrate_sde(integrator_func, df, dg, y0, t_array_timing, *args, **kwargs)

end_time = time.time()

return end_time - start_time, result[-1]

# Timing parameters

n_steps_timing = 1000

dt_timing = 0.01

timing_methods = {

'Euler': (braintools.quad.sde_euler_step, {}),

'Milstein': (braintools.quad.sde_milstein_step, {'sde_type': 'ito'}),

'Heun': (braintools.quad.sde_heun_step, {'sde_type': 'ito'}),

'SRK2': (braintools.quad.sde_srk2_step, {}),

}

times = {}

final_values = {}

print(f"Timing SDE integrators over {n_steps_timing} steps...")

for name, (method, kwargs) in timing_methods.items():

brainstate.random.set_key(jax.random.PRNGKey(42)) # Same seed for all

elapsed, final_val = time_sde_integrator(

method, gbm_drift, gbm_diffusion, y0, n_steps_timing, dt_timing,

mu, sigma, **kwargs

)

times[name] = elapsed

final_values[name] = final_val

print(f"{name:10s}: {elapsed:.4f} seconds, final value: {final_val:.6f}")

# Efficiency analysis

euler_time = times['Euler']

print("\nRelative timing (vs Euler-Maruyama):")

for name, time_val in times.items():

print(f"{name:10s}: {time_val / euler_time:.2f}x")

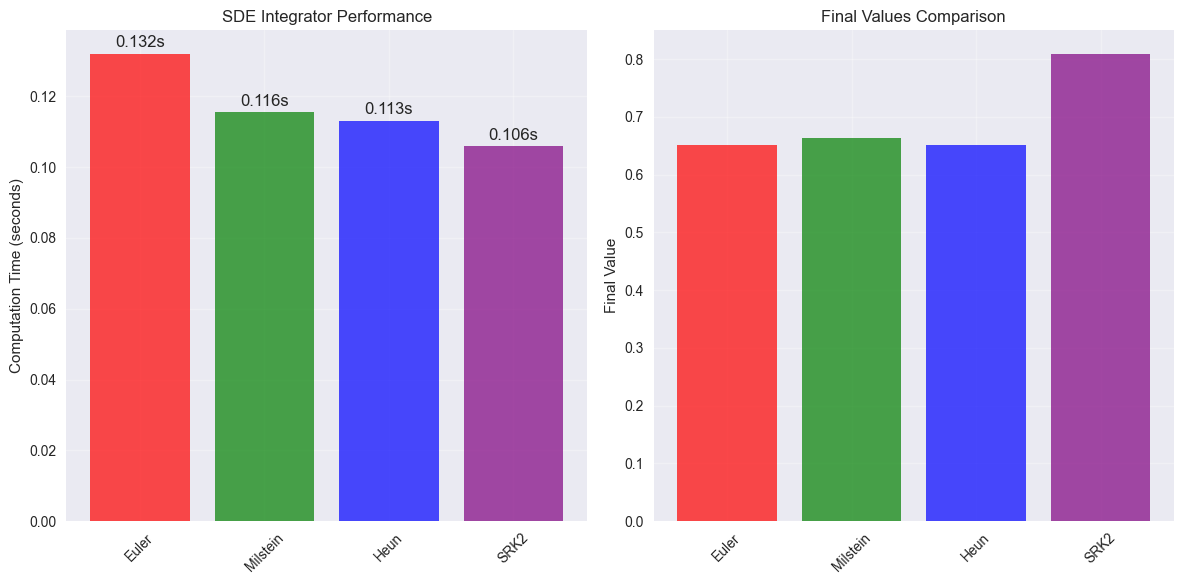

# Create performance visualization

plt.figure(figsize=(12, 6))

plt.subplot(1, 2, 1)

methods_list = list(times.keys())

times_list = [times[name] for name in methods_list]

bars = plt.bar(methods_list, times_list, alpha=0.7,

color=['red', 'green', 'blue', 'purple'])

plt.ylabel('Computation Time (seconds)')

plt.title('SDE Integrator Performance')

plt.xticks(rotation=45)

plt.grid(True, alpha=0.3)

# Add value labels on bars

for bar, time_val in zip(bars, times_list):

plt.text(bar.get_x() + bar.get_width() / 2, bar.get_height() + 0.001,

f'{time_val:.3f}s', ha='center', va='bottom')

plt.subplot(1, 2, 2)

final_vals = [final_values[name] for name in methods_list]

plt.bar(methods_list, final_vals, alpha=0.7,

color=['red', 'green', 'blue', 'purple'])

plt.ylabel('Final Value')

plt.title('Final Values Comparison')

plt.xticks(rotation=45)

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

Timing SDE integrators over 1000 steps...

Euler : 0.1320 seconds, final value: 0.651900

Milstein : 0.1155 seconds, final value: 0.662962

Heun : 0.1132 seconds, final value: 0.651795

SRK2 : 0.1059 seconds, final value: 0.809137

Relative timing (vs Euler-Maruyama):

Euler : 1.00x

Milstein : 0.87x

Heun : 0.86x

SRK2 : 0.80x

Summary#

This tutorial covered the key SDE integrators available in BrainTools:

Basic Methods:

Euler-Maruyama: Simple, strong order 0.5, weak order 1.0

Milstein: Higher accuracy with strong order 1.0

Exponential Euler: Better stability for stiff SDEs

Advanced Methods:

Stochastic Heun: Predictor-corrector scheme

Tamed Euler: Prevents explosion for superlinear growth

Implicit Euler: Enhanced stability via fixed-point iteration

SRK methods: Stochastic Runge-Kutta for Stratonovich SDEs

Key Concepts:

Itô vs Stratonovich: Different stochastic calculus interpretations

Strong vs Weak convergence: Different measures of accuracy

Noise handling: All methods use

brainstate.randomfor Gaussian noise

Guidelines:

For most problems: Use Euler-Maruyama or Milstein

For higher accuracy: Use Milstein (strong order 1.0)

For stiff problems: Try Exponential Euler or Tamed Euler

For superlinear growth: Use Tamed Euler

For Stratonovich SDEs: Consider SRK methods

BrainTools Features:

All methods work with JAX PyTrees

Global time step management via

brainstate.environConsistent random number handling via

brainstate.randomSupport for both Itô and Stratonovich interpretations

Unit-aware computations with

brainunit

Choose your SDE integrator based on the trade-off between accuracy, stability, and computational cost for your specific stochastic system.